Loading

The deal playbook

Insurance Agency M&A Blog

Expert insights on buying, selling, and valuing P&C insurance agencies.

August 5, 2026

First-Time Buyer Financing: SBA Loans, Seller Notes, and PE

Financing a first agency acquisition: SBA 7(a) loans, seller notes, and PE backing compared. A first-time buyer capital stack playbook with 2026 rates.

Read article ↗

July 29, 2026

How Insurance Agency Roll-Ups Build Value Post-Acquisition

How insurance agency roll-ups create value post-acquisition: the consolidator playbook for multiple arbitrage, integration, cross-selling, and retention.

Read article ↗

July 22, 2026

The Valuation Gap: Why Your Agency Is Worth Less Today

The valuation gap is what separates an owner's number from the buyer's number. Learn why it exists, what it costs you, and how to close it before you sell.

Read article ↗

July 20, 2026

How to Structure a Seller Carryback Note That Gets Paid

A seller carryback note is only worth what you can collect. The promissory note terms, UCC filings, and default provisions that turn paper into paid debt.

Read article ↗

July 15, 2026

How Is Rollover Equity Taxed in an Insurance Agency Sale?

How does rollover equity get taxed in an insurance agency sale? From tax-free vs. taxable rollovers to Section 1045 deferral and capital gains treatment.

Read article ↗

July 8, 2026

What a $4M Agency Sells For in 2026 (If You Even Can)

U.S. brokerage M&A delivered 241 deals through May 2026. Private capital drives 70% of deals. Here is who is buying and what multiples clear heading into Q3.

Read article ↗

July 6, 2026

Farmers.com Captive Agency Indicators: The Five to Watch

Five indicators determine a Farmers captive agency's value: retention rate, loss ratio, premium growth, policy count trend, and line-of-business mix in 2026.

Read article ↗

July 5, 2026

How to Finance an Insurance Agency Acquisition This Year

Three ways buyers finance an insurance agency acquisition in 2026: SBA 7(a) loans, commission-based lenders, and seller notes. Compare the terms and fit.

Read article ↗

July 1, 2026

How to Evaluate Allstate's Independent Agent Network

Allstate agents are exclusive contractors, not independent agents. Here is what that means for book ownership, agency valuation, and your exit strategy in 2026.

Read article ↗

June 24, 2026

What's Inside the Farmers Agent Appointment Agreement

Farmers Insurance agent appointment agreements define what you own, what you can sell, and what you walk away with. Here is how the contract actually works.

Read article ↗

June 17, 2026

Insurance Agency Valuation Calculator: Run Your Numbers

Use an insurance agency valuation calculator to estimate what your agency is worth. 2026 multiples, retention math, deal structure, and what buyers actually pay.

Read article ↗

June 10, 2026

State Farm Agent Contract Changes: What You Should Know

State Farm is overhauling compensation and benefits for 19,000 captive agents, ending AIPP, health coverage, and offering a capped buyout. Exit planning impact.

Read article ↗

June 3, 2026

Your Non-Compete Means Nothing Without Carrier Release

A non-compete means nothing if the carrier won't release the appointment. Carrier consent is the real enforcement layer in agency sales. Here's why.

Read article ↗

June 3, 2026

Rollover Equity in a Consolidator Deal: Worth the Risk?

Rollover equity in a consolidator deal means investing in a capital structure you do not control. Security class and waterfall position outweigh the percentage.

Read article ↗

May 27, 2026

The Earnout Trap: Why Your 7x Offer Pays Like a 4x

Most insurance agency earnout structures look like 7x EBITDA on the LOI and pay out like 4x in practice. Here is the math buyers do not show you.

Read article ↗

May 23, 2026

What Rollover Equity Means in an Insurance Agency PE Sale

PE-backed buyers drive 73 percent of insurance agency deals, and nearly all require rollover equity. Here is what the stake means and what to negotiate.

Read article ↗

May 20, 2026

How Long It Takes to Sell an Insurance Agency, By Stage

Selling an insurance agency takes 4 to 8 months from valuation to close. Preparation before that adds months or more. This is the full stage-by-stage timeline.

Read article ↗

May 13, 2026

Asset Purchase vs Stock Purchase: Which Costs You More?

Asset purchase vs stock purchase in an insurance agency sale: how IRS Section 1060, Form 8594, and Section 197 amortization shape buyer and seller tax outcomes.

Read article ↗

May 9, 2026

How to Prevent E&O Claims When Buying an Insurance Agency

Insurance agency M&A creates hidden E&O risks that surface months after close. Swiss Re data confirms rising claims. A prevention framework for buyers and sellers.

Read article ↗

April 29, 2026

Insurance Agency M&A Q1 2026: The Sellers Playbook

Q1 2026 OPTIS data: 148 agency M&A deals, the slowest first quarter since 2016. PE took 72 percent. What the bottoming trend means for agency sellers right now.

Read article ↗

April 22, 2026

Carrier Consent in an Insurance Agency Sale: The Rules

Carrier consent is the written permission each carrier must grant before an appointment can transfer. How it works, what carriers evaluate, how to protect the deal.

Read article ↗

April 21, 2026

Letter of Intent for an Agency Sale: What Goes In It

Seller negotiating power peaks at the LOI. Negotiate price, structure, exclusivity window, carrier-consent contingency, and non-compete before signing.

Read article ↗

April 13, 2026

Insurance Agency M&A: How Brokers Overcharge Sellers

Traditional agency M&A brokers charge 5-10 percent ($50K-$100K on a $1M sale). What you actually pay for, what brokers deliver, and better alternatives in 2026.

Read article ↗

April 6, 2026

The Tax Bill You Owe When You Sell Your Insurance Agency

Understand capital gains tax, installment sale elections, 1031 exchanges, and entity structure implications when selling your P&C insurance agency.

Read article ↗

March 30, 2026

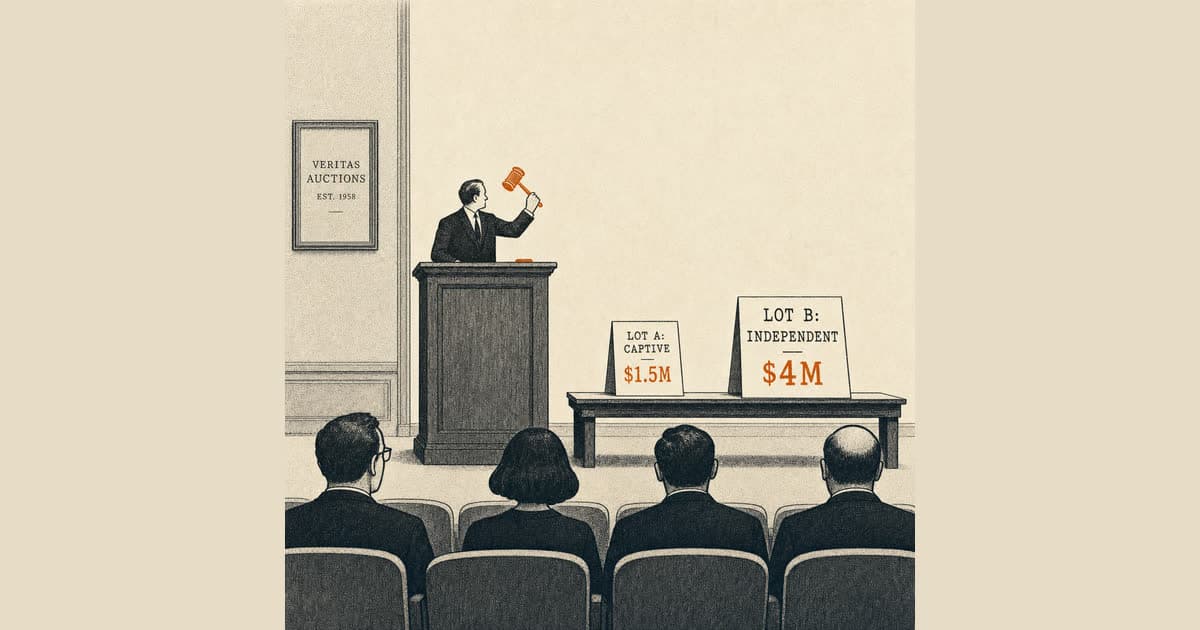

Captive vs Independent: Which Book Sells for More?

Independent P&C agencies sell for 10 to 30 percent more than captive agencies. Ownership structure, carrier flexibility, and transfer ease drive the gap.

Read article ↗

March 23, 2026

Insurance Agency Revenue Multiples 2026: What's Yours Worth?

Current market data on P&C insurance agency revenue multiples, earnings multiples, and the operating factors that move valuations up or down in 2026.

Read article ↗

March 16, 2026

Buying a P&C Insurance Agency: Where to Start First

Buyer's guide to acquiring a P&C insurance agency: financing options, due diligence checklist, retention analysis, carrier transfers, and common pitfalls to avoid.

Read article ↗

March 9, 2026

How to Sell Your Insurance Agency in 2026, Step by Step

The complete guide to selling your P&C insurance agency: preparation, valuation, listing, buyer vetting, deal structuring, and transition. Updated for 2026.

Read article ↗

March 2, 2026

Seller Carryback Financing: How Agency Sellers Get Paid

Seller carryback financing defers capital gains, earns the seller interest, and closes deals 2-3x faster than bank financing. Why it works for agency exits.

Read article ↗

February 23, 2026

How to Value a P&C Insurance Agency, Formula Included

How buyers and sellers value P&C insurance agencies: revenue multiples (1.1x-2.2x), earnings multiples (1.8x-3.7x), and the factors that move the final price.

Read article ↗

February 16, 2026

Why Farmers Agents Are Leaving in 2026, and Where They Go

Commission cuts, impossible bonus structures, and rates that haven't been competitive since 2008 - why P&C agents at Farmers are walking away from captive.

Read article ↗

February 9, 2026

Independent Agency Startup Costs Nobody Tells You About

The real numbers behind starting an independent agency, with the cost lines that matter and the ones that surprise new owners six months in.

Read article ↗

February 2, 2026

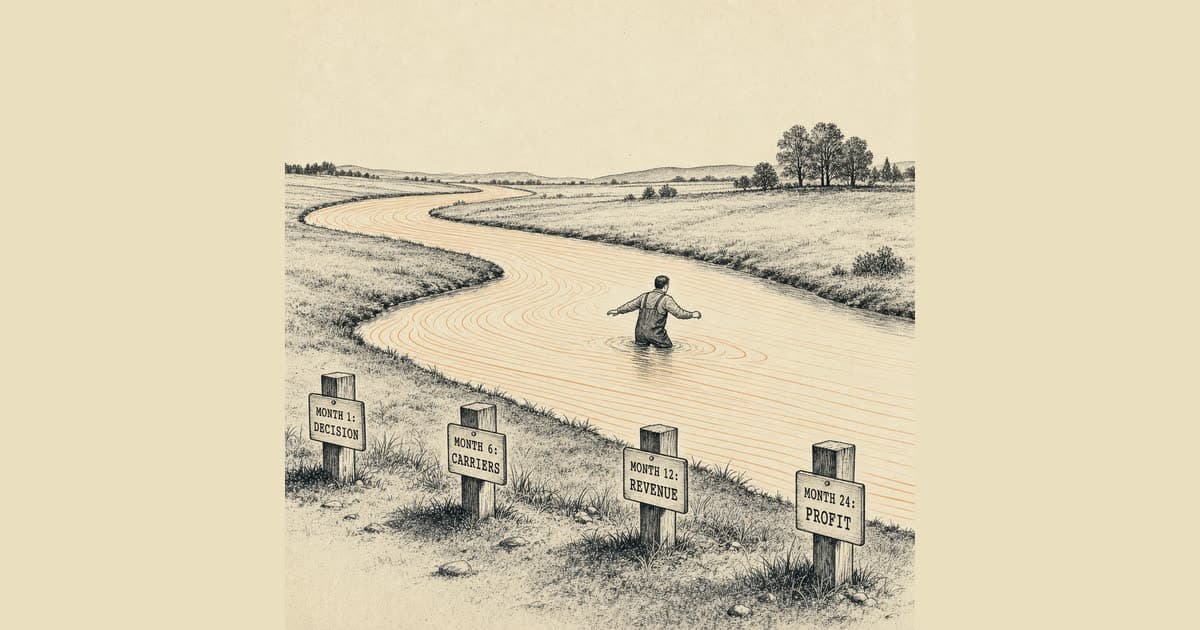

State Farm to Independent: How Long the Exit Takes

Month-by-month State Farm to independent transition: months 1-3 research, 4-6 infrastructure, 7-9 transition window, 10-12 launch and first independent clients.

Read article ↗

January 26, 2026

Captive Agent Non-Competes: What Courts Will Enforce

Captive agent non-competes restrict twelve months of direct solicitation of the former book, not all insurance practice. What holds up, what doesn't, state by state.

Read article ↗

January 19, 2026

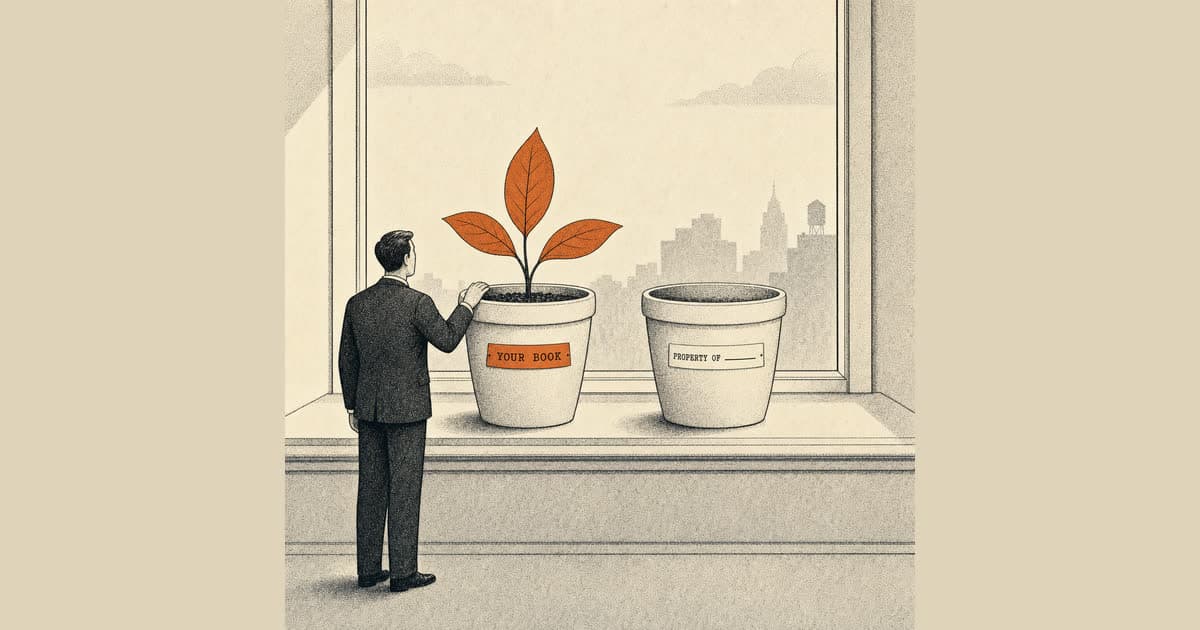

Your Book of Business Is Yours. The Agency Never Was.

The difference between owning a book of business and owning an actual business is the difference between a high-paying job and a sellable, transferable asset.

Read article ↗

January 12, 2026

I Went Independent and Finally Love Insurance Again

When you control what you do, what you sell, and who you serve, insurance stops being a grind and starts being a business you are proud of running again.

Read article ↗

January 5, 2026

How Insurance Agencies Are Valued in 2026: Inside the Math

How insurance agencies are valued in 2026: revenue multiples for captives, EBITDA multiples for independents, SDE for small agencies. Method beats the number.

Read article ↗

December 29, 2025

Why Captive Books Sell for Less Than Independent Ones

Captive books sell at 1.5 to 2.5x revenue. Independent agencies sell at 6 to 10x EBITDA. Here is why the valuation gap is structural, not negotiable.

Read article ↗

December 22, 2025

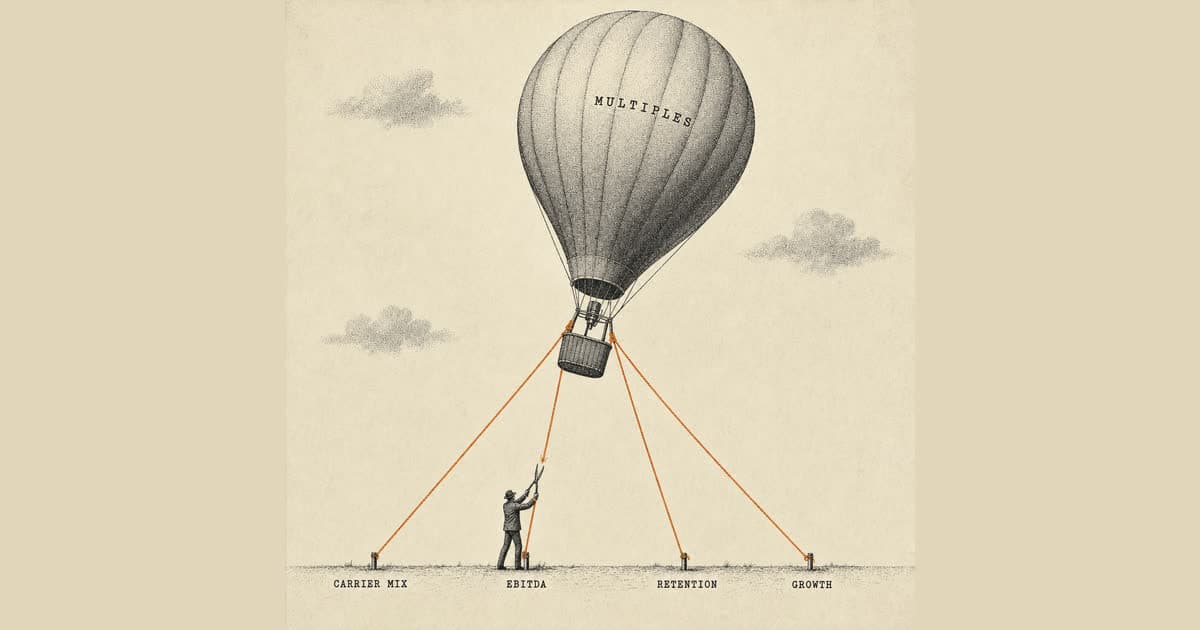

What Pushes Insurance Agency Multiples Higher Than Average

What drives insurance agency multiples from 4x to 8x EBITDA: organic growth, retention above 90 percent, EBITDA margin, owner dependency, and commercial-lines mix.

Read article ↗

December 15, 2025

What Really Happens When You Leave Allstate: The Numbers

What happens when an Allstate agent goes independent: the economic-interest buyout math, the life-insurance quota nobody warned you about, the real commission gap.

Read article ↗

December 8, 2025

The True Cost of Staying a Captive Agent, In Dollars

Most captive agents calculate the cost of leaving but never the cost of staying. A five-year projection on commission, book ownership, and enterprise value at exit.

Read article ↗

December 1, 2025

Going Independent After Ten Years Captive: Where to Start

How a veteran captive agent goes independent after ten years: the honest twelve-month timeline, the cash needed, and the non-compete reality nobody warns you about.

Read article ↗

November 24, 2025

Farmers Agent Exit Guide: What Corporate Won't Say

Farmers agents are leaving in record numbers in 2026. How the 90-day notice works, what contract value actually pays, and where the non-compete really bites.

Read article ↗

November 17, 2025

Captive vs Independent: Whose Close Ratio Wins More?

Captive agents close 7 percent of quotes; independents close 30 to 40 percent. The five-hour test, revenue-per-hour math, and what the gap costs over a career.

Read article ↗

November 10, 2025

Allstate Agents Selling Their Book: What It's Worth

Allstate restricts who you can sell to, when, and for how much. Here is what those carrier rules mean for your exit price and your transition timeline.

Read article ↗

November 3, 2025

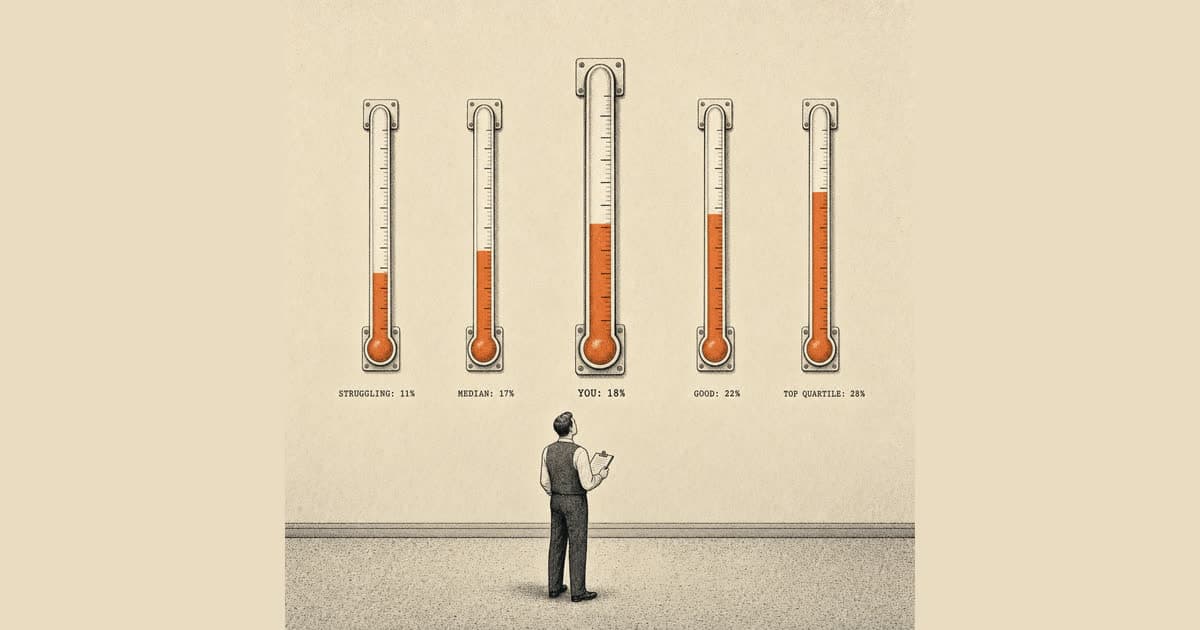

Insurance Agency EBITDA Margins: Where Do You Rank?

Insurance agency EBITDA margin benchmarks: top quartile hits 25 to 30 percent, average sits 15 to 20 percent. Where margin gets eaten and how to close the gap.

Read article ↗

October 27, 2025

Why Private Equity Pays Record Prices for Agencies

633 deals in 2024, PE-backed buyers at 73.5 percent of all agency transactions. Here is what that buyer mix means for your agency's likely sale price and terms.

Read article ↗

October 20, 2025

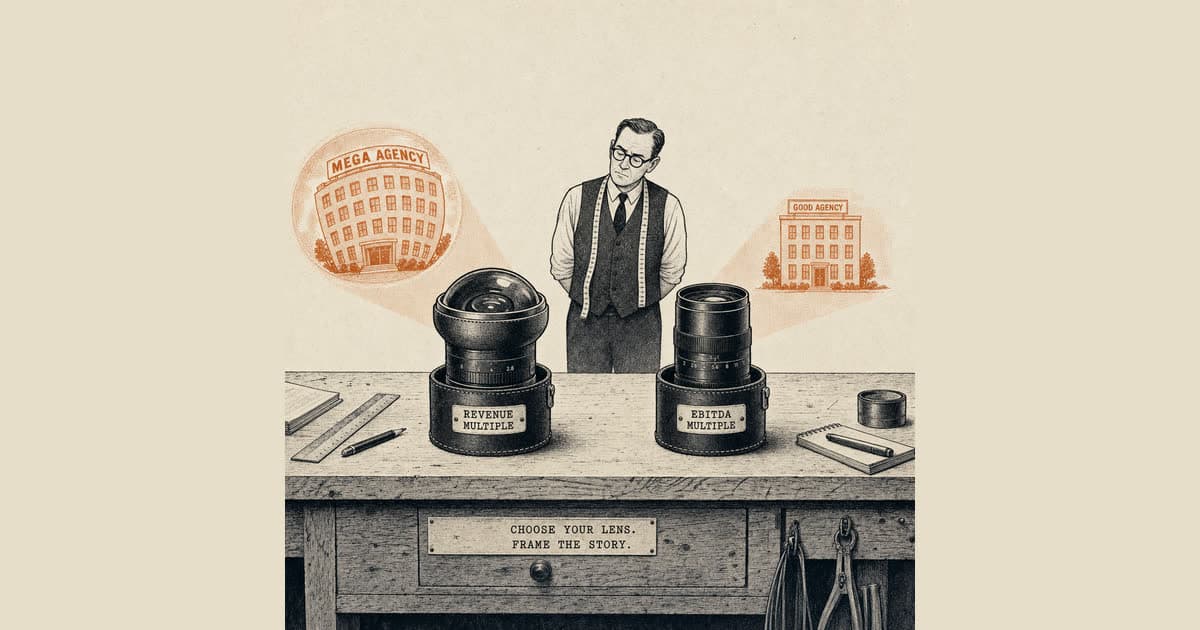

Revenue Multiple vs EBITDA Multiple: Which Should You Use?

Revenue multiples vs EBITDA multiples: why two agencies at $10M revenue can be worth twice apart. Normalization, capture rate, and seller bargaining power.

Read article ↗

October 13, 2025

5 Agency Valuation Mistakes That Cost You Six Figures

Most agency owners have no idea what their business is actually worth, and the 5 mistakes here are the ones that cost owners six figures at sale time.

Read article ↗

October 6, 2025

What Buyers Look For First When Acquiring an Agency

What agency buyers actually evaluate: organic growth rate, retention above 90 percent, EBITDA margin, technology stack, client concentration, owner dependency.

Read article ↗

September 29, 2025

Buying an Insurance Book of Business: The Full Guide

What to evaluate, what to pay, and what to watch for when buying an insurance book of business: retention, carrier mix, customer concentration, producer dependency.

Read article ↗

September 22, 2025

How to Finance an Insurance Agency Acquisition, No Cash

How insurance agency acquisitions actually get financed: SBA 7(a) loans, seller carryback (cheapest), earnouts, and PE platform partnerships for $5M+ deals.

Read article ↗

September 15, 2025

The Due Diligence Checklist Before You Buy an Agency

Due diligence on an agency purchase: 20 verifications across financials, retention, loss ratios, carrier relationships, and the walkaway list every buyer needs.

Read article ↗

September 8, 2025

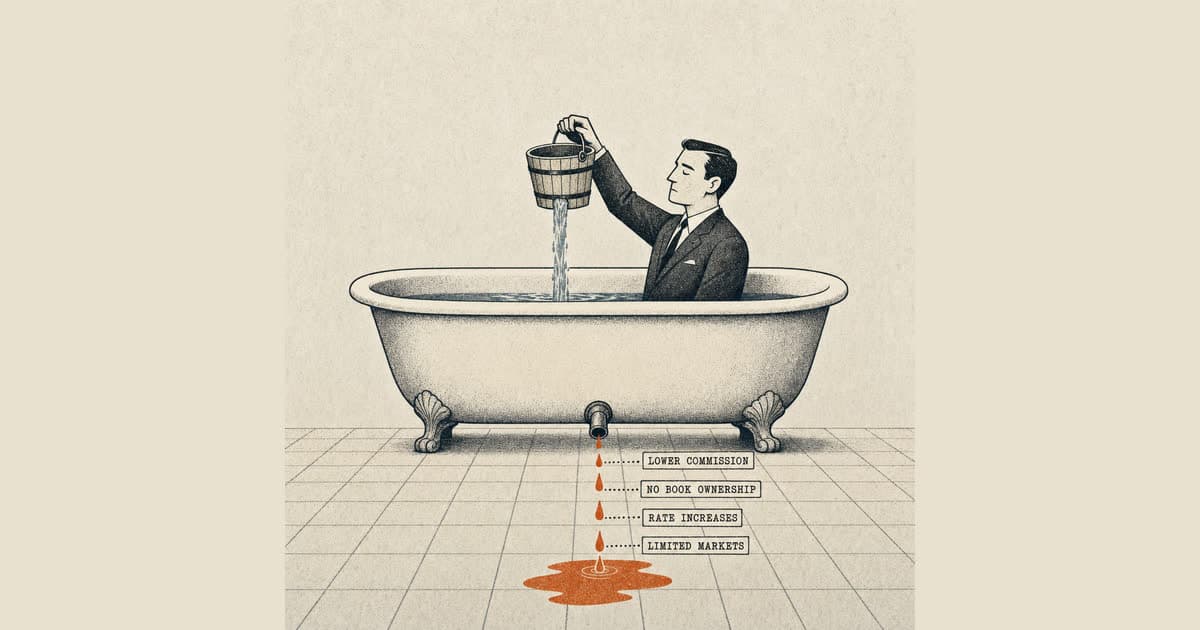

Why Retention Rate Matters Most When Buying an Agency

A 95 percent retention rate and an 85 percent retention rate look similar on paper. The difference at closing is hundreds of thousands of dollars in agency value.

Read article ↗

September 1, 2025

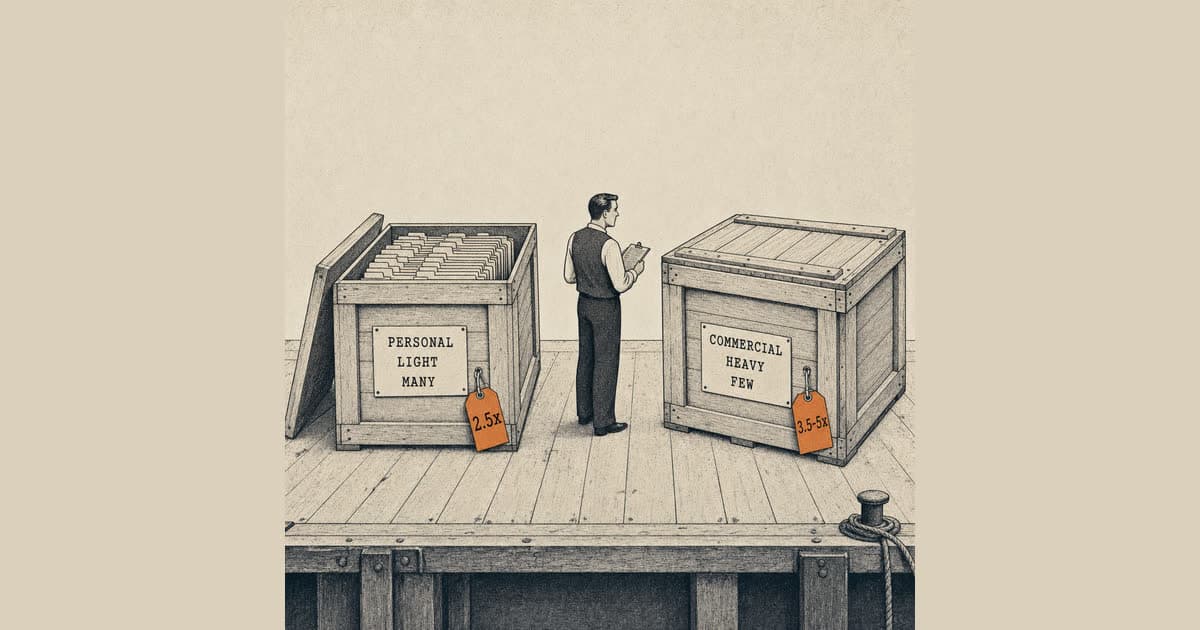

Personal Lines vs Commercial: Which Wins When Buying?

Commercial books command higher multiples but personal lines books are easier to operate at scale. Here is the math on which one to buy if given the choice.

Read article ↗

August 25, 2025

Your First Year After Buying an Agency: What to Expect

Nobody talks about the integration chaos, the 6 AM client calls, or the carrier renegotiations. Here is what your first year as a new owner looks like.

Read article ↗

August 18, 2025

Buying an Agency vs Starting From Scratch: The Math

Starting from scratch sounds noble. Buying an existing book sounds expensive. Here is the real math on which path actually wins for your time and capital.

Read article ↗

August 11, 2025

When Is the Right Time to Sell Your Insurance Agency

Timing the sale of your agency is worth hundreds of thousands. Here is how to know when the market favors you and which signals predict the next price ceiling.

Read article ↗

August 4, 2025

How to Prepare Your Agency for Sale: The 3 Year Plan

The agencies that sell for top dollar did not get lucky. They spent three years getting their books, their systems, and their team buyer-ready before the listing.

Read article ↗

July 28, 2025

Selling to Private Equity vs an Independent Buyer, Compared

Selling to PE vs an independent buyer: PE pays higher multiples but loads earnouts. Independent buyers pay less but close cleaner with cash and full exit.

Read article ↗

July 21, 2025

Earnout Structures: How Not to Get Burned on the Sale

Earnouts can add 30 to 40 percent to your sale price or leave you working for free for two years. Here is how to structure them so the upside is real.

Read article ↗

July 14, 2025

Tax Implications of Selling Your Agency: What Changes

The difference between asset sale and stock sale tax treatment can be six figures on a $1M deal. Know the structure and the elections before you sign the LOI.

Read article ↗

July 7, 2025

The 7 Deal Killers That Blow Up an Agency Sale Cold

Most failed agency sales die for preventable reasons. Here are the seven that kill deals most often, with the early warning signs and the fixes that save the close.

Read article ↗

June 30, 2025

Do You Need a Broker to Sell Your Agency? Maybe Not

Agency brokers charge 5-10 percent of the sale. When that fee is worth it ($5M+ deals, no time), when you can go direct, and how to negotiate if you hire one.

Read article ↗

June 23, 2025

Insurance Agency Succession Planning: The Full Roadmap

The best exit starts a decade early. Here is the succession planning framework that maximizes your payout, protects your team, and keeps the agency intact post-sale.

Read article ↗

June 16, 2025

Internal Perpetuation vs External Sale: Which Pays More?

Selling to your team preserves your legacy and your culture. Selling externally maximizes your payout. Here is how to decide which path actually fits your goals.

Read article ↗

June 9, 2025

Buy-Sell Agreements: The Insurance Agency Clause You Need

A funded buy-sell is the most important doc in your agency. Most owners do not have one funded properly. The gap costs heirs hundreds of thousands.

Read article ↗

June 2, 2025

How to Develop Next-Gen Leadership in Your Agency Now

Your agency value depends on not depending on you. Here is how to build the team and the systems that make you operationally optional before the buyer's first call.

Read article ↗

May 26, 2025

Agency Owner Burnout: When It Is Time to Walk Away

If you dread Monday mornings and your book runs you instead of the other way around, the numbers are already telling you it's time to consider an exit.

Read article ↗

May 19, 2025

What Happens to Your Agency If You Die Without a Plan

Morbid question, critical answer. Most agencies lose 30 to 50 percent of their value within 90 days of an owner death without a funded buy-sell agreement in place.

Read article ↗

May 12, 2025

AMS Comparison for Agencies: EZLynx vs HawkSoft vs Applied

Your agency management system is the backbone of your operation. Here is how to choose between EZLynx, HawkSoft, and Applied without regret or migration pain.

Read article ↗

May 5, 2025

Carrier Appointments: How New Independent Agents Land Them

How new independent agents get carrier appointments: the 12-24 month direct timeline, aggregator shortcuts (SIAA, Smart Choice, PGI), and carrier sequencing.

Read article ↗

April 28, 2025

How to Build a Referral Network as an Independent Agent

Independent agents who grow fastest do not buy leads. They build referral networks that feed clients in at zero acquisition cost, by design and discipline.

Read article ↗

April 21, 2025

Hiring Your Agency's First Employee: The When and How

When to hire your first agency employee: the revenue trigger ($200K-$250K), why your first hire must be a CSR not a producer, and the virtual-assistant bridge.

Read article ↗

April 14, 2025

Insurance Agency Marketing Budget: What New Agencies Spend

Fast-growing agencies spend 10 to 15 percent of revenue on marketing. Most new agents spend 2 percent. Where the budget goes and the brand-recognition gap.

Read article ↗

April 7, 2025

E&O Insurance for Independent Agents: What It Covers

Your errors and omissions coverage is the foundation of your independent practice. Here is what to buy, what to skip, and what the policy actually costs in 2026.

Read article ↗

March 31, 2025

Nationwide Went Independent. Is Your Carrier Next?

The captive model is dying as carriers admit. Nationwide's transition to independent distribution is just the loudest example of an industry-wide shift.

Read article ↗

March 24, 2025

Will Direct to Consumer Insurance Kill Local Agents?

GEICO and Progressive are growing. Lemonade exists. But independent agents are not going anywhere if they pivot to advisor work where the carriers cannot reach.

Read article ↗

March 17, 2025

Why a Hard Market Is Good News for Independent Agents

When rates harden, captive agents lose clients while independents capture the dissatisfied book. Hard markets deliver double the new business to independents.

Read article ↗

March 10, 2025

Insurance Consolidation in 2026: Where Small Agencies Fit

Big is getting bigger and PE is rolling up agencies at record pace. Here is what small independent owners need to know about positioning to survive or sell into it.

Read article ↗

March 3, 2025

How Insurtech Is Changing Independent Agencies in 2026

How insurtech actually helps independent agents: AMS upgrades, quoting engines, AI underwriting, and the tech-stack premium buyers pay for. Real threat isn't tech.

Read article ↗

February 24, 2025

Insurance Agent Career Outlook 2026: What's Changing

Insurance agent career outlook 2026: agents aren't dying, the captive model is. Where the age-wave opportunity and independent channel growth are actually heading.

Read article ↗

Ready to buy or sell an agency?

Get started with our free tools or browse active listings.