Why Captive Books Sell for Less Than Independent Ones

Captive books sell at 1.5 to 2.5x revenue. Independent agencies sell at 6 to 10x EBITDA. Here is why the valuation gap is structural, not negotiable.

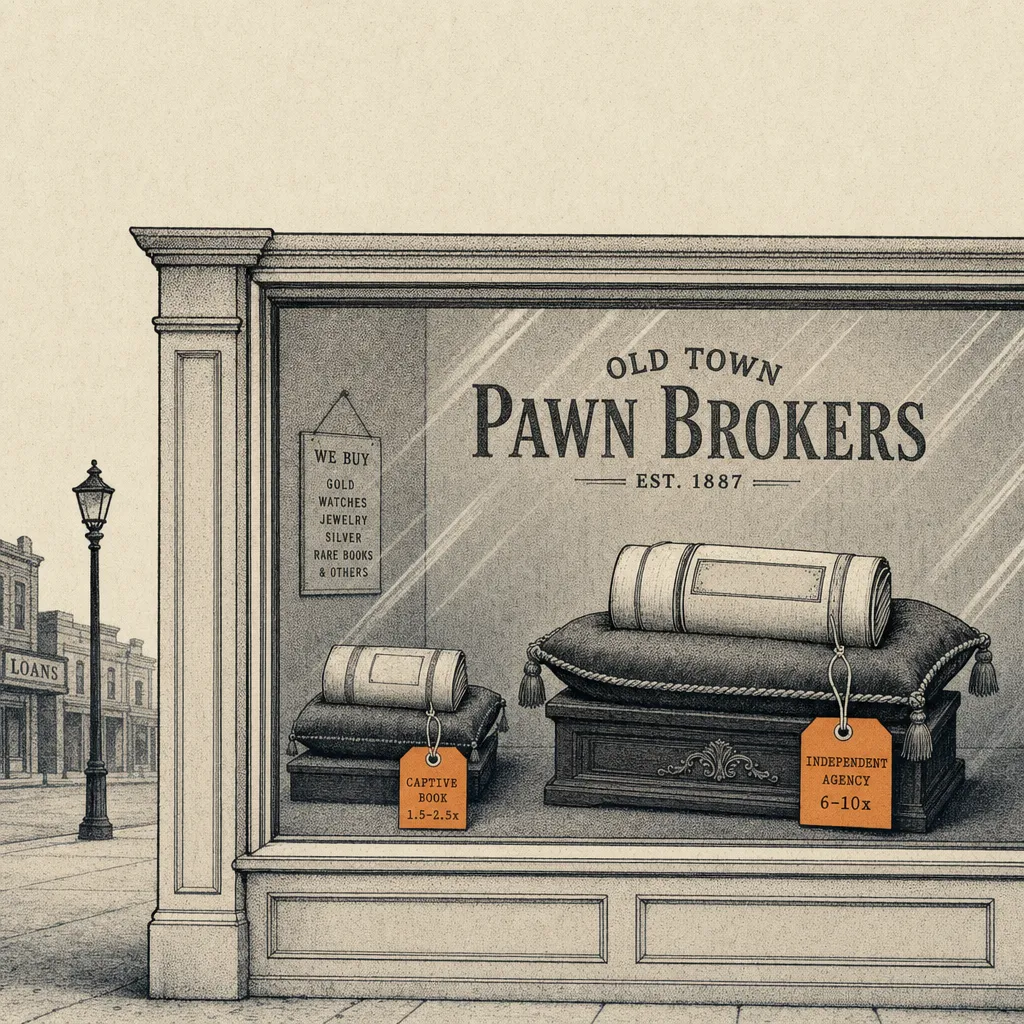

Captive books typically trade at 1.5x to 2.5x revenue. Independent agencies trade at 6x to 10x EBITDA. The gap reflects ownership of expirations, carrier transferability, and the structural restrictions on who can buy a captive book. The same revenue produces vastly different exit numbers.

You've been building your book for fifteen years. You've hit your quotas, survived the commission cuts, handled the rate increases. You've earned every policy in that book through blood, sweat and more cold calls than you want to remember.

So it's going to sting when I tell you what it's actually worth.

What Does the Captive Sale Math Actually Look Like?

A captive book of business typically sells at 1.5 to 2.5 times annual revenue. Let's say you're doing $400,000 a year. Your book is worth somewhere between $600,000 and $1,000,000. Sounds reasonable until you understand the constraints.

You can only sell to a buyer your carrier approves. Your carrier controls the terms. The buyer pool is limited to other agents within that system or sometimes to the carrier itself. This isn't a free market transaction, it's a controlled one and controlled markets produce lower prices.

The buyer knows that every policy in your book is with a single carrier. If that carrier raises rates, changes underwriting appetite or decides to push direct-to-consumer and all three of those things are happening right now, the buyer has no hedge. They're buying concentrated risk tied to a single entity's decisions.

MarshBerry reports that independent firms with strong profitability trade at multiples ranging from the mid-single digits to mid-teens, while captive books face structural discounts due to carrier-controlled ownership of expirations and transfer approval requirements.

Allstate's agent count has dropped to just 8,400, down from 9,300 a year prior and 10,400 two years ago, according to SEC filings reported by Insurance Business Magazine. Allstate agents accounted for only 38% of new auto policies in 2022, down from 71% in 2020.

Farmers has been cutting base commission rates "for most products" while restructuring its agent distribution model, prompting what agents on Indeed describe as "commissions reduced to the point of theft."

What Does the Independent Sale Math Look Like for Comparable Revenue?

An independent agency with $400,000 in revenue and a 20 percent EBITDA margin produces $80,000 in annual earnings. At a conservative 7 times EBITDA multiple, that agency is worth $560,000.

Wait, that's less than the captive book.

Not so fast. The independent agency at $400,000 in revenue is positioned for stronger organic growth due to the close ratio advantage of multi-carrier access. That same agency two years from now might be doing $550,000 with improving margins. At 25 percent EBITDA margin on $550,000, you're at $137,500 in earnings. At 8 times which is normal for a growing independent agency, that's $1,100,000.

The captive book two years from now? Probably $420,000 in revenue, valued at $840,000 on a good day. Same starting point, widening gap.

Why Does the Captive-vs-Independent Valuation Gap Exist?

Captive books are valued on revenue because there's no real business to value. You don't control your carrier mix, your pricing, your commission structure or your growth strategy. You're selling a customer list attached to one company's products.

Independent agencies are valued on earnings because they are real businesses. You control costs, carrier relationships, product mix and growth strategy. Buyers are purchasing a profit-generating machine, not just a list of names.

This distinction matters because it changes everything about how you build over the next decade. Every dollar of revenue you add as a captive agent increases your book value by $1.50 to $2.50. Every dollar of EBITDA you add as an independent agency owner increases your enterprise value by $6 to $10.

What Is the Restricted-Sale Problem for Captive Books?

Even setting aside the valuation math, captive agents face a structural problem when selling: you can't always sell to the highest bidder. Your carrier has approval rights. Some carriers restrict sales entirely, forcing you to find a buyer within their agent network.

An independent agency owner can sell to anyone, another independent agent, a PE firm, a strategic acquirer, a cluster group or a competitor. More buyers means more competition which means higher prices. This isn't theoretical, it's basic supply and demand applied to your life's work. See how to value a P&C insurance agency for the underlying earnings-based math.

Non-compete enforceability varies significantly by state. California prohibits them entirely, while states like North Carolina have upheld Allstate's enforcement of non-solicitation agreements. The FTC's proposed ban on non-compete agreements (April 2024) remains in legal limbo, though non-solicitation agreements are explicitly excluded.

"Allstate agents are contracted to sell and service Allstate Insurance policies... unlike true independent contractor insurance agents, captive Allstate agents are prohibited from performing their profession with any other insurance carrier." NAPAA (National Association of Professional Allstate Agents), Attorney General Letter

What Is the Twenty-Year Question for Captive Agents?

If you're ten years into a captive career, you've got roughly ten to fifteen years of building left before you want to exit. That's ten to fifteen years of enterprise value creation or not.

Building within a captive system means your book grows linearly with your revenue, capped by a single carrier's rates and appetite. Building as an independent means your agency value grows exponentially with your earnings and margins, amplified by competitive buyer demand.

Same agent. Same work ethic. Same market. Fundamentally different asset at the end.

The numbers don't care about loyalty. They don't care about your relationship with your district manager. They care about cash flow, growth and optionality. On all three counts, the independent model produces structurally different outcomes, a reality that captive agents increasingly factor into their long-term planning. Every agent's situation is different and any transition involves navigating contract restrictions, non-competes and financial trade-offs that require professional guidance.

Your book isn't what you think it's worth. It's worth what a restricted market says it's worth. And that restricted market isn't doing you any favors. If you do decide to exit, our captive-to-independent transition guide lays out the realistic path.

Frequently Asked Questions

Q: Can I sell my State Farm agency?

A: Not on the open market. State Farm agents are independent contractors, but the agent agreement routes book assignment back through the company, you can't list it, auction it or sell it to the highest bidder. Any "sale" is an internal process which is the main reason State Farm books rarely trade at independent-style multiples.

Q: How much will Allstate pay me for my TPP?

A: The Termination Payment is a formula-driven calculation under your R3001 contract, not a market price. Agents on forums routinely report the TPP is materially less than a negotiated sale to an Allstate-approved buyer which is why most exit-planners pursue a sale rather than taking the TPP.

Q: How is my Farmers contract value calculated?

A: Farmers contract value is tied to your commission history and production, not to what a buyer would pay for an equivalent independent book. After the commission restructuring, agents have reported lower-than-projected payouts which is part of why Farmers churn is elevated, see why Farmers agents are leaving.

Q: If I have ten years left, is it worth going independent?

A: For most agents under 55, the compounding difference between a capped revenue multiple and an EBITDA-based enterprise value more than offsets the 12-18 month transition dip. The right answer depends on your specific contract, state law and financial runway, professional review before acting is essential.

Sources & References

- Insurance Business Magazine: Allstate Agent Count Drop

- NAPAA: Allstate Agent Classification

- Wallace Miller: Allstate Class Action

- The Insurer: Farmers Commission Cuts

- Insurance Journal: Allstate v. Robbins (NC) non-compete enforcement

- AgencyEquity: FTC Non-Compete Rule

- MarshBerry: Valuation Guide

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.