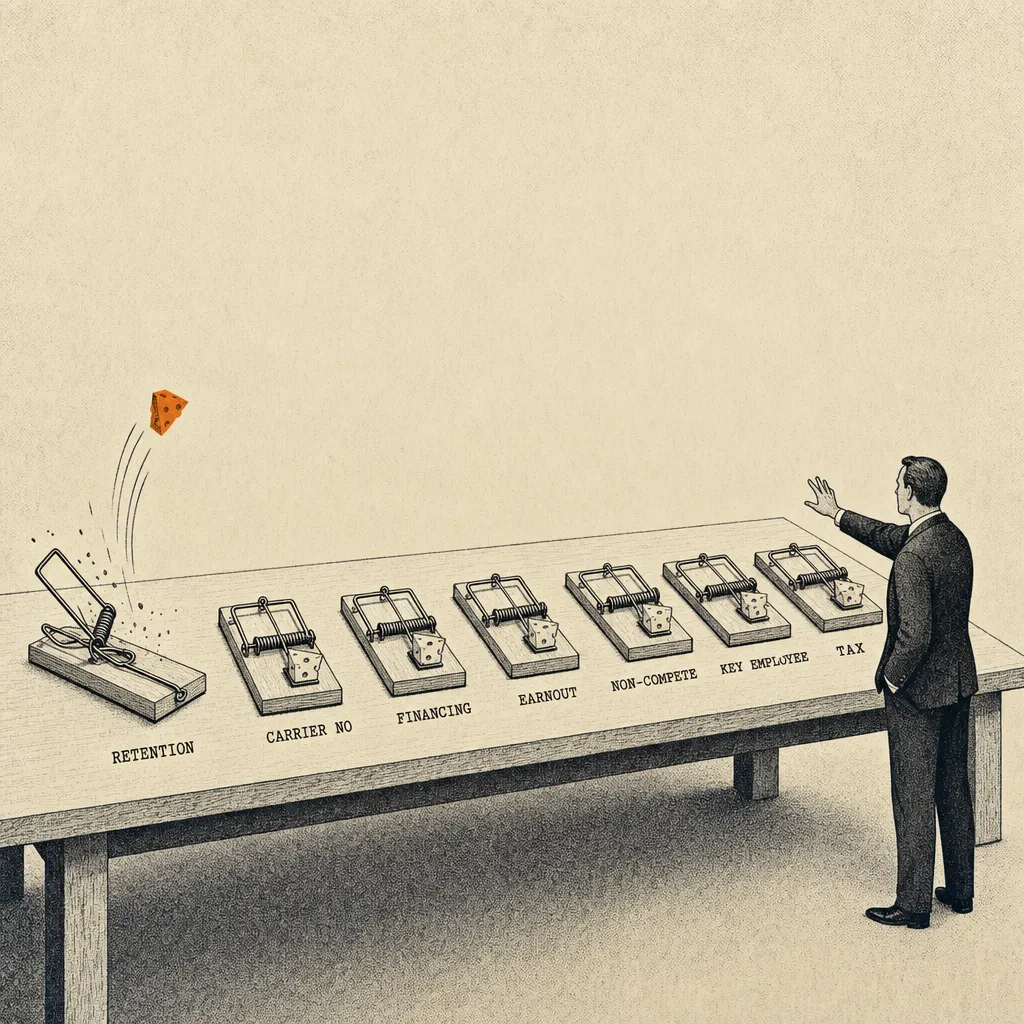

The 7 Deal Killers That Blow Up an Agency Sale Cold

Most failed agency sales die for preventable reasons. Here are the seven that kill deals most often, with the early warning signs and the fixes that save the close.

Seven deal-killers blow up agency sales most often: customer concentration above 10 percent, owner dependency, messy financials, declining retention, unrealistic price expectations, fragile carrier relationships, and staff exodus during due diligence. Each is preventable with three years of preparation. None are fixable inside an active deal.

Most agency sales that fall apart don't die from some unexpected catastrophe. They die from problems that were sitting in plain sight, problems the seller could have fixed if they'd started earlier.

Here are seven deal killers that M&A advisors and transaction data consistently highlight as the most common causes of failed agency sales.

1. Why Does Customer Concentration Kill Agency Deals?

If your top client represents 15 percent of your revenue, acquirers will stress-test what happens if that client leaves. MarshBerry identifies client concentration as a primary valuation discount factor, and in many buyer models, concentrated risk is assumed to materialize, because concentrated risk is the first thing an acquirer stress-tests.

The fix takes time. You can't diversify a concentrated book in six months. You need two to three years of deliberate new business development focused on building a broader client base. Start now.

2. Why Does Owner Dependency Spook Every Sophisticated Buyer?

The buyer asks: "What happens if you leave?" If the honest answer is "the agency struggles significantly," the deal either dies or gets restructured with an unfavorable earnout.

Owner dependency means the key client relationships, the carrier contacts, the operational knowledge, and the sales engine all live in your head. Buyers aren't paying enterprise-value multiples for a job. They're paying for a machine that runs without the previous operator.

3. How Do Messy Financials Sink Otherwise Clean Deals?

Personal expenses on the books, inconsistent accounting methods, missing records, and unexplainable fluctuations in revenue or expenses all create doubt. Doubt kills deals faster than bad numbers, because bad numbers can be understood. Messy numbers can't be trusted.

M&A advisors recommend three years of clean, normalized financials as the standard for agency transactions. If you can't produce that, expect lower offers, longer due diligence, and higher probability of the buyer walking.

4. Why Does Declining Retention End a Deal Mid-Diligence?

A declining retention trend (even from 94 percent to 91 percent over three years) signals a book that's getting less sticky. Buyers project that trend forward and price accordingly. A book that's at 91 percent and declining might be at 87 percent in two years, which changes the economics of the acquisition entirely. (MarshBerry's benchmarking research places top-tier agency retention above 93 to 94 percent, meaning a slide to 91 percent already signals an underperforming book relative to the agencies commanding premium multiples. [1])

If your retention is dropping, figure out why before you go to market. Rate-driven losses might stabilize. Service-driven losses are fixable. If you don't know why retention is declining, a buyer will assume the worst.

5. How Do Unrealistic Price Expectations Kill the Deal Before It Starts?

Sellers who have an inflated sense of their agency's value (usually because they heard what someone else sold for without understanding the differences) waste everyone's time. Buyers make offers based on data, and if expectations are significantly above market, the deal often never reaches a letter of intent.

Get a professional valuation before you go to market. If the number disappoints you, spend two to three years improving the fundamentals before listing. Don't spend six months in a deal process that was never going to close because your expectations and reality couldn't be reconciled. Review common valuation mistakes so you're not the one making them.

6. What Carrier-Relationship Risks End Deals at Consent Stage?

If a key carrier is about to non-renew a block of business, restrict new business in your market, or has communicated dissatisfaction with your loss ratios, the buyer will find out during due diligence. Surprises about carrier stability are deal killers because they introduce uncertainty into the revenue model.

Resolve carrier issues before going to market. If a carrier relationship is genuinely at risk, address it or disclose it upfront. Buyers can price known risks. They can't price surprises.

7. Why Does Staff Exodus During Due Diligence Detonate the Deal?

Due diligence takes three to six months. During that time, your staff might learn the agency is being sold. Some will start looking for other jobs. Key people leaving during the process terrifies buyers because those people take client relationships with them. (OPTIS Partners' deal tracking data (covering 750-plus transactions in 2024) and MarshBerry's M&A advisory experience both reflect that extended due diligence windows of three to six months are standard for mid-market agency transactions, underscoring why staff communication and retention plans must be in place before the process begins. [2] [3])

Manage the communication carefully. Don't announce the sale prematurely. Have retention plans (whether bonuses, employment agreements, or equity participation) ready for your most critical staff. The buyers will ask what you've done to retain key people, and "nothing" is the wrong answer.

What Is the Common Thread Across All Seven Deal-Killers?

Every one of these deal killers shares the same root: lack of preparation. The seller waited too long, ignored known problems, or went to market without understanding what buyers evaluate and how.

The deal that closes at a premium multiple is the deal where none of these problems exist, not because the seller was lucky, but because they spent years making sure they wouldn't be. The 3-year preparation playbook is how you get there, and what buyers actually look for tells you exactly what acquirers will stress-test.

Frequently Asked Questions

Q: What are the most common reasons deals fall apart?

A: Messy financials, undisclosed client concentration, surprise carrier issues, declining retention, and owner dependency discovered during due diligence. Buyers can price a known risk. They can't price a discovered one, so disclose proactively.

Q: Should I tell my staff I'm selling?

A: Not prematurely. Announce only when necessary (typically during due diligence or post-LOI), and have retention plans (bonuses, employment agreements) ready for your most critical staff. Losing a key producer mid-deal is a classic deal-killer.

Q: Can I sell my agency if retention is declining?

A: Yes, but at a discount. Buyers project the trend forward and price accordingly. If retention dropped for a specific, fixable reason, diagnose it before listing so you can explain the turnaround story to buyers.

Q: Why did my agency come in lower than I expected?

A: Often it's something buyers discover in diligence: a key producer leaving, client concentration, carrier issues, or personal expenses run through the P&L. See agency valuation mistakes for what to clean up 3+ years before listing.

Q: How much client concentration is too much?

A: Any single client above 5-10% of revenue triggers concentration discounts. Above 15%, acquirers stress-test what happens if the client leaves post-close and often price in the loss as a near-certainty.

Sources & References

- MarshBerry: How to Think About Value

- OPTIS Partners / Insurance Journal: P&C and Benefits Brokerage M&A - 750+ Deals in 2024

- Sica Fletcher: Insurance Agency Valuation Rule of Thumb

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.