The True Cost of Staying a Captive Agent, In Dollars

Most captive agents calculate the cost of leaving but never the cost of staying. A five-year projection on commission, book ownership, and enterprise value at exit.

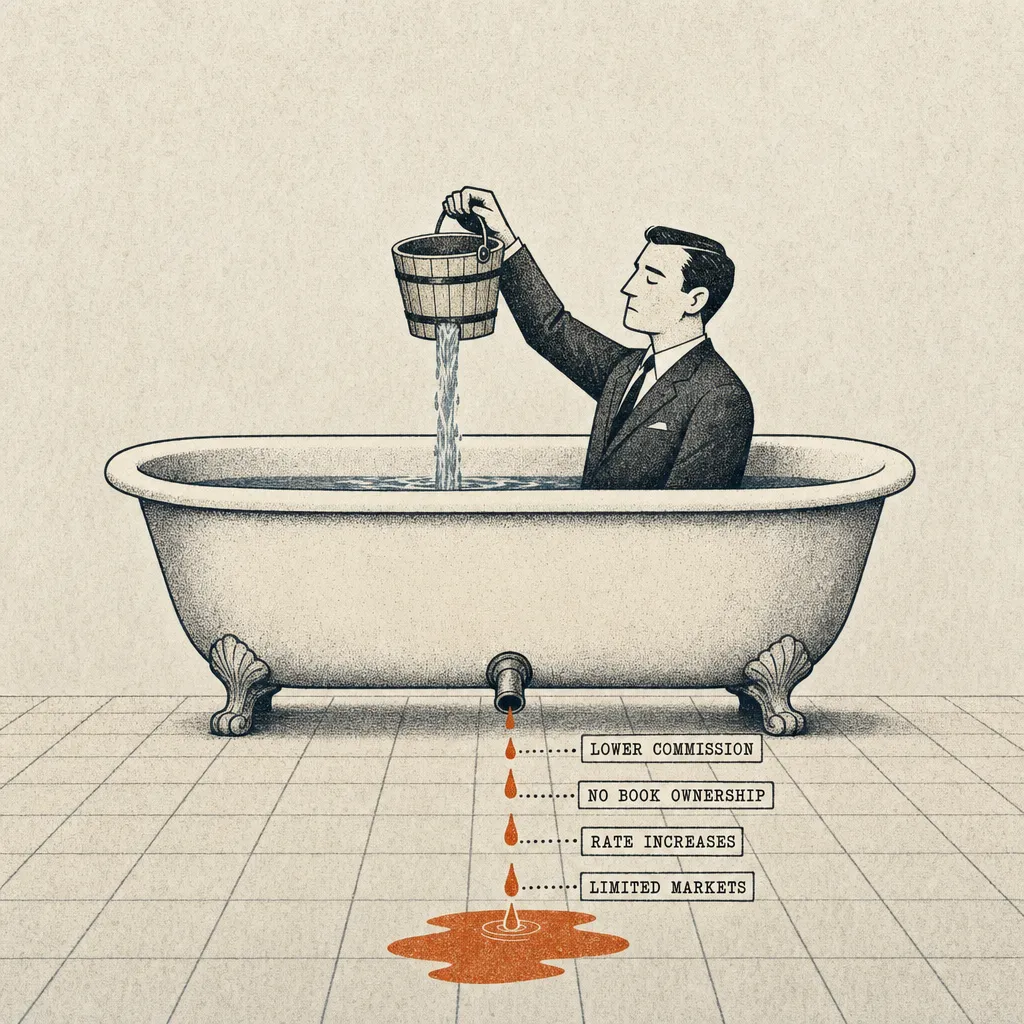

Captive agents reliably price the cost of leaving and ignore the cost of staying. Over five years the gap compounds in lower commission rates, no real book ownership, weaker close ratios, and a missing enterprise value at exit. The cheaper-looking path almost never wins on paper.

Most captive agents think about the cost of leaving. The transition expenses, the income dip, the uncertainty. Those costs are real and I'm not going to pretend they aren't.

But almost nobody calculates the cost of staying.

Let me run a five-year hypothetical projection using industry benchmarks and you tell me which option is more expensive.

What Does a Captive Agent's Year One Actually Look Like?

Let's say you're a captive agent generating $300,000 in annual revenue. Let's assume you're running at about 60 percent efficiency after expenses, a figure many captive agents would consider reasonable. That gives you roughly $180,000 in take-home before taxes.

Not bad. That's a good living and it's the number your district manager will point to when you bring up going independent.

Now let's look at what that same $300,000 in revenue looks like as a captive asset. Using the standard captive book multiple of 1.5 to 2.5 times revenue, your book is worth somewhere between $450,000 and $750,000. (Peak Business Valuation; Sica Fletcher) Let's split the difference and call it $600,000.

That's your retirement asset. Your twenty years of effort. Your equity. Six hundred thousand dollars.

How Does Year One Compare on the Independent Side?

In this hypothetical, an independent agent with $300,000 in revenue might run at 40 to 45 percent net efficiency, lower than captive because you're paying for your own tech stack, E&O and carrier management overhead. But the growth trajectory is fundamentally different because the close ratio advantage of multi-carrier access is substantial.

The more important number: your independent agency at $300,000 in revenue with a 20 percent EBITDA margin produces $60,000 in EBITDA. At an EBITDA multiple of 7 times, conservative for the current market, your agency is worth $420,000. (Insurance Journal notes that agencies under $2M EBITDA typically trade at 8-10x, making 7x a floor rather than a ceiling.)

Wait, that's less than the captive book.

Yes. At $300,000 in revenue, the captive book might actually be worth more on paper. This is where the projection gets interesting.

Where Do the Captive and Independent Paths Diverge in Years Two Through Five?

In this projection, the captive agent at $300,000 in revenue grows at 3 to 5 percent per year, a pace consistent with the constraints of a single-carrier close ratio. After five years, revenue reaches $350,000 to $370,000. Book value at 2 times revenue: roughly $700,000 to $740,000.

The independent agent starts at the same $300,000 but is positioned for stronger growth due to the close ratio advantage of multi-carrier access. In this projection, after five years that agency reaches $600,000 to $900,000 in revenue, though actual growth depends on market conditions, execution and individual factors.

EBITDA at 25 percent margin on $750,000 revenue: $187,500. At a 7x multiple: $1,312,500.

The captive agent grew their asset from $600,000 to $740,000 in five years. The independent agent grew from $420,000 to over $1.3 million. And that independent multiple could easily be 8 or 9 times in today's market, pushing the value over $1.5 million. The underlying math is laid out in why your captive book is worth a fraction of an independent agency.

Why Does the Enterprise Value Gap Keep Widening Every Year?

Here's what makes this particularly brutal: the gap accelerates. The captive agent's growth is capped by carrier restrictions and a single-product close ratio. The independent agent's growth compounds because every new client relationship creates cross-sell opportunities, referral possibilities and carrier diversification.

Extending this projection to year ten illustrates how the gap compounds, though these are hypothetical figures, not market guarantees. The structural difference between revenue-based captive valuations and EBITDA-based independent valuations means the models diverge further over time.

What Costs of Staying Captive Never Show Up on a Spreadsheet?

The financial projection tells one story. The quality-of-life projection tells another.

Five more years as a captive agent means five more years of production requirements set by your carrier, commission structures that can change at the carrier's discretion, competitive pressures from your own carrier's direct channel and the constant knowledge that 90 percent of the people who ask for your help leave empty-handed.

Five years as an independent means you choose your carriers, set your own goals, build equity that you control and help the vast majority of people who walk through your door. Not all of them, but most of them.

The agents who've made the switch don't talk about the money first. They talk about the feeling of actually being able to help their clients. The frustration of turning people away because your only carrier was too expensive, that goes away. And it turns out that when you can actually help people, the money follows.

What Are the Carriers Already Telling You About Your Future?

Nationwide converted its captive agents to an independent model. American Family is now available through independent agents. Allstate acquired National General in 2021 to service the independent channel and NAPAA reports that independent commission rates through National General exceed captive Allstate rates. Nationwide's captive-to-independent conversion is well-documented in industry coverage. Allstate's acquisition of National General in 2021 created an independent distribution platform and Insurance Business Magazine reports that Allstate's exclusive agent count has dropped to record lows as the company shifts toward direct and independent channels.

The carriers themselves are betting on the independent model. When the companies that built the captive system are actively building independent distribution channels, the writing isn't on the wall, it's on the earnings call.

What Is the Real Five-Year Cost of Staying Captive?

This projection illustrates the potential enterprise value difference between the two models over a five-year period, though actual results depend on market conditions, individual execution and factors that vary by agent and region.

The structural differences between these models compound over time, a pattern that agents factor into their long-term planning. Any transition involves contract restrictions, non-compete clauses and financial trade-offs that require professional guidance from an attorney who specializes in insurance agency contracts. For the practical path forward, see how to go independent after ten years captive.

"There is a general pullback in the pace of acquisition for more than half of the historically most-active buyers." Steve Germundson, OPTIS Partners (Insurance Journal)

Frequently Asked Questions

Q: Will I make more as an independent?

A: Most agents report higher total income within 18-24 months because multi-carrier close ratios run 3-4x captive rates and commissions are uncapped. The compounding difference over 5-10 years is what agents on forums mean when they say "I wish I'd left sooner."

Q: Is my captive carrier next?

A: No one can predict specific announcements, but the industry has clearly shifted, Nationwide converted fully and several major carriers operate parallel independent channels. Staying captive on the assumption that nothing will change is itself a decision with financial consequences.

Q: What's the worst that can happen if I leave my captive carrier?

A: The realistic downside is a 12-18 month income dip and non-solicitation enforcement exposure if you contact former clients during the restricted period. Catastrophic outcomes agents worry about on forums are uncommon when the transition is planned with counsel and funded adequately.

Q: Doesn't captive give me a "guaranteed" income?

A: Captive income is carrier-controlled, not guaranteed, commission restructurings (Farmers 2023), bonus formula changes and rate non-competitiveness can reduce captive earnings with little notice. "Guaranteed" captive income is really "stable until the carrier changes it."

Q: If I'm close to retirement, should I still switch?

A: Usually not. The transition valley typically consumes 12-18 months of productivity, so agents within five years of retirement are often better off optimizing retention and pursuing a carrier-approved sale. See when to sell your insurance agency for timing frameworks.

Sources & References

- Peak Business Valuation: Valuation Multiples for an Insurance Agency

- Sica Fletcher: Insurance Agency Valuation Rule of Thumb

- Insurance Journal: EBITDA Multiples in Agency M&A

- Insurance Business Magazine: Allstate Agent Count Drops to Record Low

- Nationwide Agency Forward: Succession Planning for Insurance Agencies

- OPTIS Partners: 750 Deals Report via Insurance Journal

- MarshBerry: Insurance Brokerage M&A Activity 2024

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.