Selling to Private Equity vs an Independent Buyer, Compared

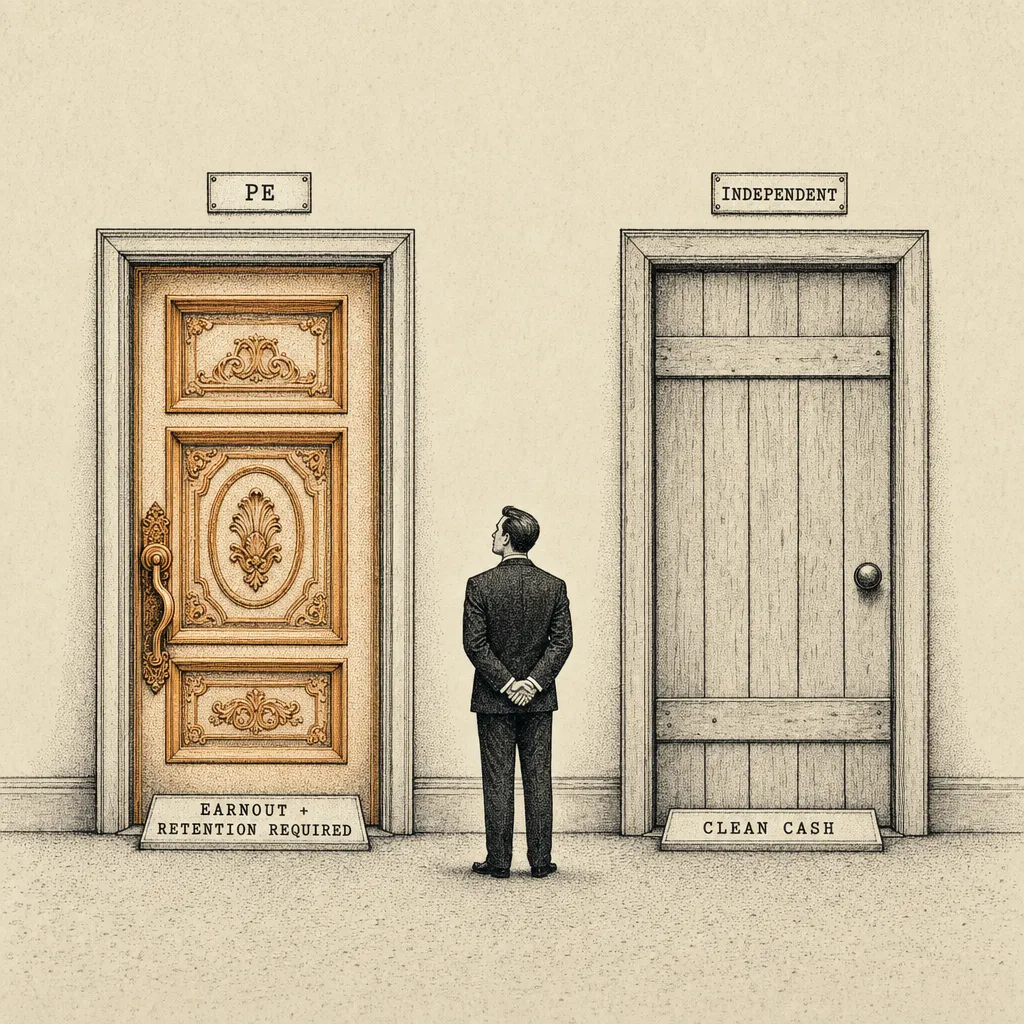

Selling to PE vs an independent buyer: PE pays higher multiples but loads earnouts. Independent buyers pay less but close cleaner with cash and full exit.

PE pays higher headline multiples but loads earnouts, retention requirements, and operational control onto the seller. Independent buyers pay less upfront but close cleaner with cash and exit you completely. The decision turns on whether you want maximum dollars or maximum freedom from the deal.

When it's time to sell your agency, the buyer pool breaks into two distinct camps: private equity-backed acquirers and independent buyers. The experience of selling to each is fundamentally different, and the right choice depends on what you value beyond the check.

What Does a Typical PE Offer Look Like?

PE-backed acquirers typically offer higher headline numbers. They have access to institutional capital, they're competing with other PE firms for quality assets, and their model depends on acquiring at multiples that attract good agencies.

The structure is where PE gets complicated. A typical PE deal might look like this: 60 to 70 percent of the purchase price paid at close, with the remaining 30 to 40 percent tied to an earnout over two to three years. The earnout is usually based on retention targets and sometimes growth targets. (MarshBerry's deal structure analysis confirms this pattern: the majority of PE-backed transactions in insurance brokerage close with a significant deferred component, with PE involvement accounting for 73.5 percent of all announced deals in 2024. [1])

PE buyers also frequently want the seller to stay on for a transition period, often one to three years, based on industry transaction patterns. During that time, you're running the agency under new ownership, hitting targets, reporting to someone, and managing the cultural integration. For some sellers, this is fine. For others, it's the opposite of what they wanted when they decided to sell. For the broader list of what PE and strategic acquirers evaluate before they make an offer, see what buyers actually look for.

The upside: if you hit your earnout targets, total compensation can exceed what any independent buyer would have paid. PE firms also sometimes offer equity rollover. You retain a minority stake in the combined platform, which can pay off enormously if the PE firm executes its roll-up strategy and exits at a higher multiple. For the mechanics of PE earnouts, see earnout structures explained.

What Does a Typical Independent Buyer Offer Look Like?

Independent buyers (typically other agency owners looking to expand) generally offer lower headline numbers but cleaner deal structures. Based on industry transaction patterns, independent buyer deals tend to involve a higher percentage of cash at close with a simple seller note for the balance and fewer complex earnout provisions.

Transition periods tend to be shorter with independent buyers. The buyer is typically local, understands the market, and plans to run the agency personally, which agents report tends to produce smoother staff transitions.

The trade-off is price. Independent buyers can't match PE multiples because they're financing personally, not with institutional capital. Where PE might offer 8 times EBITDA, an independent buyer might offer 6 times. On a $200,000 EBITDA agency, that's a $400,000 difference, before you factor in the earnout risk on the PE side. (Sica Fletcher's benchmarks corroborate this spread: PE-backed buyers routinely price quality agencies above 7x to 8x EBITDA, while independent buyers cluster in the 5x to 7x range. [2] OPTIS Partners tracked over 750 announced M&A transactions in 2024, the majority of which involved PE-backed platforms bidding at premium multiples. [3])

Which Emotional Factors Tip the PE-vs-Independent Decision?

Numbers aside, there's an emotional dimension that most sellers underestimate. Your agency is twenty years of your life. Your staff are people you care about. Your clients trust you.

Selling to PE means your agency becomes a business unit in a larger platform. Agents who've sold to PE platforms report that branding changes, process standardization, and centralized decision-making are common post-close dynamics. Some sellers are fine with this. The premium they received justifies the change. Others watch the transformation and feel like they sold something precious to someone who doesn't appreciate it.

Selling to an independent buyer often feels more like a passing of the torch. The buyer is building something of their own, they care about the community, and they're personally invested in the agency's success. The lower price comes with the comfort of knowing your life's work is in hands that understand what it represents.

Which Decision Framework Picks the Right Buyer Type?

Sell to PE if you want maximum total compensation and are willing to work through an earnout period, your agency meets the size threshold that typically attracts PE interest (industry participants report this is generally $250K+ EBITDA, though it varies by platform), and you're comfortable with corporate integration and cultural change.

Sell to an independent if you want a clean break with cash at close, you value what happens to your staff and clients post-sale, your agency is below the PE threshold, or you simply don't want to work for someone else during a transition period.

Neither option is wrong. But choosing the wrong one for your personality and priorities can turn the biggest payday of your career into a regret you can't undo.

Know what you're optimizing for before you take the meeting. The buyers will know what they're optimizing for. For context on the broader PE push into insurance distribution, read why private equity is paying record prices for insurance agencies.

Frequently Asked Questions

Q: Should I sell to PE or an individual buyer?

A: PE headline prices are typically higher (8x+ EBITDA vs. 6x for independents), but 30-40% of PE consideration is often tied to earnouts over 2-3 years, plus a longer post-close commitment. Independent buyers usually pay less upfront but offer simpler deal terms and shorter transitions.

Q: What's the difference between PE and strategic buyer offers?

A: PE offers higher headline multiples with more complex structures (earnouts, equity rollover, 1-3 year retention). Strategic/independent buyers typically offer lower multiples but simpler cash-plus-seller-note structures and 60-90 day transitions. Compare the net-to-seller after risk, not just the headline number.

Q: How much will I actually net after taxes and fees?

A: With PE, assume 30-40% is at-risk earnout and factor in 20-23.8% federal capital gains. Strategic buyer structures with seller carryback convert to installment-sale treatment and spread the tax over the payment period. Run both scenarios in our seller strategy tool.

Q: How long do PE buyers want me to stay post-close?

A: Typically 1-3 years. You report to the platform, hit targets, and manage cultural integration. Independent buyers usually want shorter transition periods (60-90 days) and no long-term commitment.

Q: Will PE change the agency after buying it?

A: Almost always. Branding, processes, and decision-making typically centralize. If preserving the agency's identity and community relationships matters to you, an independent buyer may be a better cultural fit even at a lower price. See PE firms buying insurance agencies for how PE roll-ups actually operate.

Sources & References

- MarshBerry, Insurance Brokerage M&A Activity: 2024 Year-End Review

- Sica Fletcher, Insurance Agency Valuation Rule of Thumb

- OPTIS Partners / Insurance Journal, P&C and Benefits Brokerage M&A: 750+ Deals in 2024

- Deloitte, Insurance M&A Outlook

When Does an Earnout From a PE Buyer Actually Make Sense?

When the earnout is tied to retention metrics inside your control and the multiple on the base is already at the top of the market. Earnouts tied to growth targets you cannot influence post-close are a discount disguised as upside.

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.