Earnout Structures: How Not to Get Burned on the Sale

Earnouts can add 30 to 40 percent to your sale price or leave you working for free for two years. Here is how to structure them so the upside is real.

Earnouts add 30 to 40 percent to the sale price or leave the seller working unpaid for two years. The structure that protects you specifies retention or growth metrics, caps the buyer's downside, and includes acceleration clauses for early hits.

If you're selling your agency to a PE-backed buyer (and increasingly to larger independent acquirers), the word "earnout" will appear in the offer letter. It can be the best part of the deal or the worst. The difference is in the structure.

How Do Earnouts Actually Work in an Agency Sale?

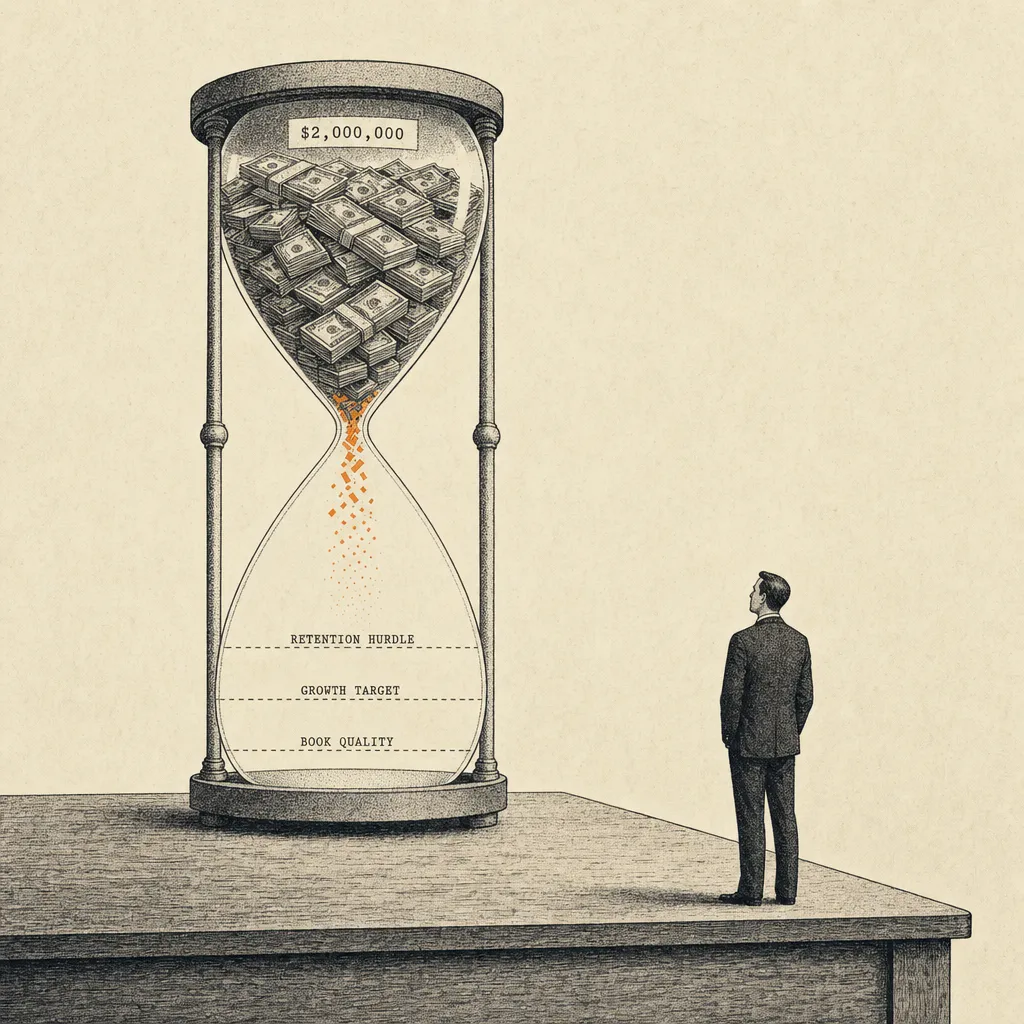

An earnout defers a portion of the purchase price and ties it to the agency's post-close performance. Typical structure: 60 to 70 percent of the total price at close, with 30 to 40 percent paid over two to three years based on hitting defined targets. MarshBerry's deal structure analysis confirms this split is the dominant earnout structure in independent agency M&A transactions.

If you're selling for $2 million with a 70/30 earnout, you get $1.4 million at close and up to $600,000 over the next two to three years, if the targets are met. If they're not, that $600,000 evaporates, and your actual sale price was $1.4 million.

Which Retention-Based Earnout Structures Protect Both Sides?

The most common and fairest earnout structure is retention-based. Typical structures tie full earnout payment to retention at or above a defined threshold, with proportional decreases below it. MarshBerry's benchmarking data shows that 90 to 93 percent retention is the threshold most acquirers use to evaluate book quality during due diligence and earnout measurement.

Retention earnouts work because retention is measurable, both parties understand it, and the seller can influence it through a smooth transition. See why retention rate is the only number that matters when buying an agency for why this is the fairest earnout benchmark. They also protect the buyer against the book shrinking after closing, which is a legitimate risk.

The danger with retention earnouts is the definition. Retention calculated by policy count is different from retention by premium volume. If the buyer raises rates aggressively post-close and some clients non-renew, was that your retention failure or their pricing decision? Define the measurement method explicitly in the purchase agreement.

Which Growth-Based Earnout Structures Pay the Seller for Upside?

Growth earnouts tie payments to the agency hitting revenue or premium growth targets post-close. These are riskier for sellers because growth depends on factors increasingly outside your control after you've sold: marketing investment, carrier appetite, staff hiring, and strategic decisions the buyer makes.

If you're staying on to run the agency during the earnout period and you have authority over growth-related decisions, a growth earnout can be lucrative. If you're in an advisory role with limited authority while the buyer makes the real decisions, a growth earnout is a trap.

How Do You Protect Yourself From Earnout Manipulation?

Structure matters more than headline number. Insist on clear, objective, measurable targets. Quarterly measurement periods with documented reporting. An independent dispute resolution mechanism. Protection against the buyer sabotaging performance through rate increases, staffing changes, or resource withdrawal.

The strongest protection is a retention floor: below a certain retention percentage, the earnout adjusts, but above it, the payment is guaranteed regardless of other factors. This limits your downside while keeping the buyer's interest in retention aligned with yours.

Also negotiate what happens if the buyer resells the agency during your earnout period. If a PE firm buys your agency and then sells the platform eighteen months later, does your earnout transfer? Does it accelerate? Get this in writing. Our seller carryback financing guide covers the financing side of deal structure that often pairs with earnouts.

When Should You Walk Away From an Earnout-Heavy Offer?

Before you accept an earnout structure, do the walk-away math. If you get zero earnout (everything goes wrong post-close), is the cash-at-close amount acceptable? If $1.4 million at close would make you happy even if you never see the additional $600,000, the deal works. If you need the full $2 million to make the economics worthwhile, you're banking on performance targets in a business you no longer control.

The best mindset for earnouts: the cash at close is the real price. The earnout is a bonus if things go well. If you can live with that framework, the earnout structure is fine. If you can't, negotiate for more cash at close and less earnout, even if the headline number is lower.

A guaranteed $1.6 million is worth more than a potential $2 million that depends on someone else's decisions for the next three years. Before you evaluate any offer structure, make sure you understand how to sell your insurance agency in 2026 and the tax consequences of an agency sale.

This post is informational only. Consult an M&A attorney and CPA before agreeing to any earnout structure.

Frequently Asked Questions

Q: How do earnouts actually work?

A: An earnout defers 30-40% of the purchase price and ties it to post-close performance measured over 2-3 years. You get 60-70% cash at close, then quarterly or annual true-ups based on hitting retention or revenue targets. If targets are missed, the deferred portion evaporates, so structure matters more than the headline number.

Q: Can I protect myself from an earnout that depends on the buyer?

A: Yes, but only if you negotiate protections upfront: a retention floor that locks in the earnout regardless of other factors, quarterly measurement with documented reporting, an independent dispute resolution mechanism, and explicit language preventing buyer-driven sabotage (aggressive rate hikes, staff cuts, resource withdrawal). Without these, growth earnouts are a trap once you no longer control decisions.

Q: Are retention-based or growth-based earnouts better for sellers?

A: Retention-based, almost always. Retention is measurable, both parties understand it, and the seller can influence it through a smooth transition. Growth earnouts depend on post-close factors the seller no longer controls (marketing investment, staffing, strategic direction), which makes them far riskier.

Q: How is retention measured in an earnout, by policy count or premium?

A: Whatever the purchase agreement says. Policy count and premium can diverge significantly if the buyer raises rates aggressively post-close. Define the measurement method explicitly: "retention of in-force premium as of closing, measured on the anniversary date, calculated as X divided by Y." Ambiguity always favors the party writing the check.

Q: What happens to my earnout if the buyer resells the agency?

A: Unless the purchase agreement addresses it, your earnout could evaporate. Negotiate an acceleration clause: if the agency is sold during your earnout period, the remaining earnout becomes immediately payable or transfers to the new owner at full value. PE-backed buyers in particular flip platforms regularly. Plan for it.

Sources & References

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.