Personal Lines vs Commercial: Which Wins When Buying?

Commercial books command higher multiples but personal lines books are easier to operate at scale. Here is the math on which one to buy if given the choice.

Commercial-lines books command higher multiples but require commercial-grade producer talent and longer renewal cycles. Personal-lines books trade at lower multiples but spin faster and integrate cleaner. The right answer depends on your existing infrastructure, your buyer pool, and your exit timeline.

The first acquisition decision most new independent agents face is deceptively simple: do I buy a personal lines book or a commercial lines book? The answer shapes your agency's trajectory for the next decade.

When Does a Personal-Lines Book Make Sense for a Buyer?

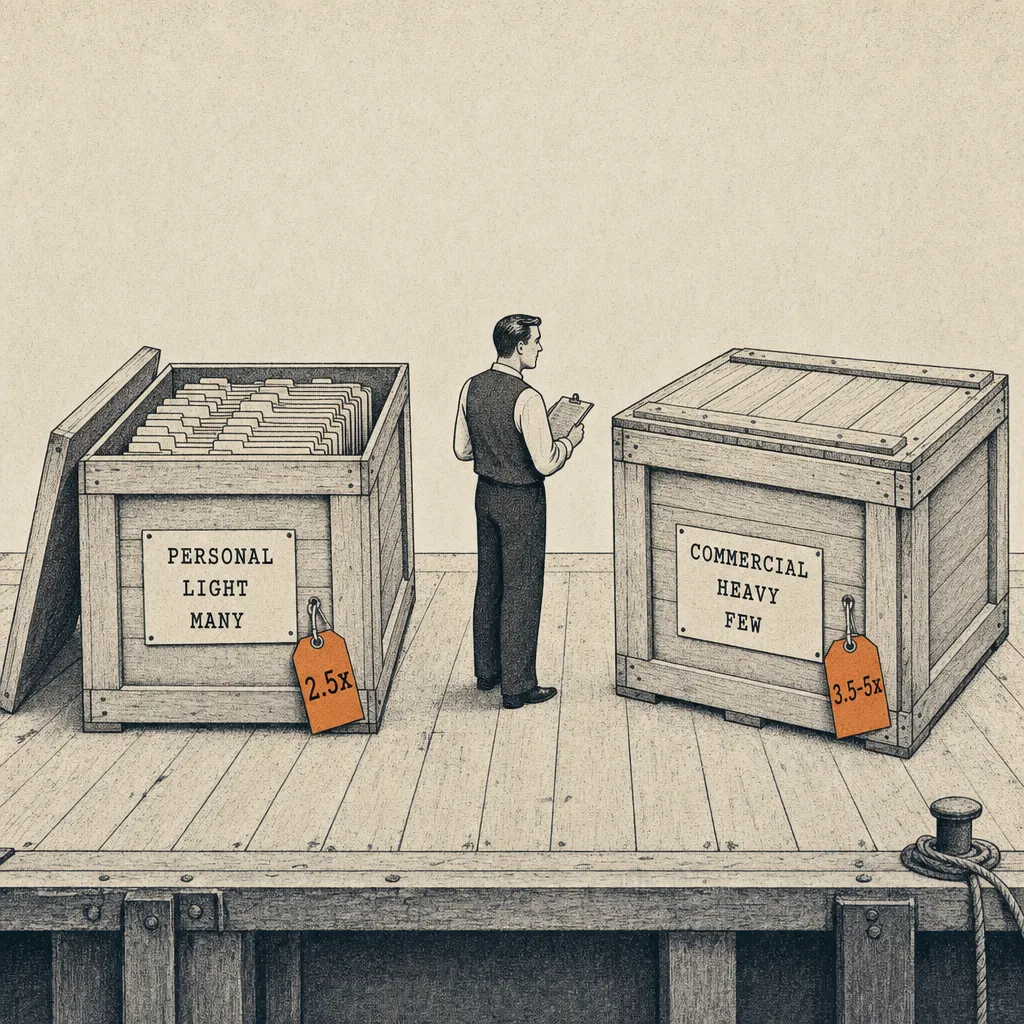

Personal lines books (auto, home, renters, umbrella) are the bread and butter of most agency acquisitions. They're plentiful because most retiring agents built personal lines practices. They're straightforward to operate because the coverage is standardized and the underwriting is automated.

Pricing: personal lines books typically trade at 1.5 to 2 times annual commission. A book producing $200,000 in annual commission might sell for $300,000 to $400,000. For current transaction data, see our roundup of insurance agency revenue multiples in 2026. The multiples are lower because personal lines clients are more transactional and more price-sensitive. When rates increase, a percentage of them will shop. That churn suppresses the premium buyers will pay. (Peak Business Valuation's brokerage multiple data confirms this personal lines pricing band, noting that lower retention and higher price sensitivity are the primary factors compressing multiples relative to commercial lines. [1])

The operational upside is real, though. Generally, personal lines operations are more straightforward to staff. A trained CSR can handle much of the servicing. The technology tools are mature. Comparative raters make quoting fast. If you're buying your first book and want something manageable while you learn the business, personal lines is the lower-risk entry point.

When Does a Commercial-Lines Book Justify the Premium?

Commercial lines books (business owners policies, general liability, workers comp, commercial auto, professional liability) command higher multiples for good reason. Revenue per account tends to be higher, relationships tend to be stickier, and client switching costs are greater, dynamics that Sica Fletcher and MarshBerry cite as primary drivers of the commercial lines valuation premium.

A commercial lines book might sell at 2 to 3 times annual commission. The same $200,000 in commission revenue could cost $400,000 to $600,000. You're paying more because the retention is better, the cross-sell opportunities are deeper, and the clients are less likely to switch over a $50 price difference. (Sica Fletcher's benchmarking confirms the commercial premium: commercial-focused books consistently transact at the higher end of the commission multiple range, driven by superior retention and account complexity. [2] OPTIS Partners' deal data across 750-plus 2024 transactions reflects that commercial-weighted agencies attract the most competitive bidding from both PE-backed and strategic acquirers. [3])

The challenge is complexity. Commercial accounts require real underwriting knowledge, carrier negotiations, and relationship management that personal lines doesn't demand. You need staff who understand coverage, not just people who can process applications. If you don't have commercial lines experience, buying a commercial book is like buying a restaurant when you can't cook. Our due diligence guide covers the extra diligence that commercial books require.

Where Does the Niche Premium Come From in Specialty Books?

Within commercial lines, specialty niches command the highest multiples. Books concentrated in contractors insurance, transportation, professional liability for specific professions, or hospitality can command premium multiples above the standard commercial range. These niches are valuable because the expertise creates a barrier to entry. Clients can't just switch to any agent because not every agent understands their industry.

If you're going to specialize, pick an industry you understand or are willing to become expert in. The learning curve is steep but the economics are compelling. In the current M&A market, niche expertise is one of the strongest multiplier drivers. Specialized agencies can command valuations that exceed larger generalist operations.

How Does a Balanced Personal-Commercial Book Compare?

The agencies that command the highest acquisition multiples from PE and strategic buyers tend to have books with meaningful commercial components. The personal lines provide volume and stable renewal income. The commercial lines provide margin, retention, and growth potential.

If you're acquiring your first book and it's purely personal lines, that's fine as a starting point. But your three-year plan should include building or acquiring commercial capability. Acquirers evaluating agencies for acquisition consistently weight commercial lines mix as a valuation factor, per MarshBerry and OPTIS Partners transaction data.

Which Decision Framework Should You Use to Pick a Book Type?

Buy personal lines if you're new to independent agency ownership, want operational simplicity, have limited capital for acquisition, and plan to grow into commercial over time. Buy commercial lines if you have industry experience, can afford the higher purchase price, have staff who understand the coverage, and want to build premium enterprise value faster.

The worst move is buying commercial lines because the multiples are better and then struggling to service the book because you don't have the expertise. A well-run personal lines book is worth more than a poorly-run commercial one every single time.

Buy what you can run well. Then build toward what you want to own. Whatever you pick, get the valuation framework right before making an offer.

Frequently Asked Questions

Q: Is personal lines or commercial a better book to buy?

A: Depends on your experience and capital. Personal lines is the lower-risk entry point: standardized coverage, automated underwriting, trained CSRs can handle most servicing. Commercial requires real underwriting knowledge and carrier relationships but commands higher multiples and better retention. New independent agents typically start personal and build toward commercial.

Q: Should I buy personal lines or commercial first?

A: Start with what you can actually run. A well-run personal lines book is worth more than a poorly-run commercial one every single time. If you've never serviced a BOP or a workers comp account, buying a commercial book is buying a restaurant when you can't cook.

Q: Why do commercial insurance books command higher multiples?

A: Three reasons: higher revenue per account, stickier client relationships, and higher switching costs. Commercial clients don't shop over a $50 savings the way personal lines clients will. Better retention and deeper cross-sell translate directly into higher multiples: typically 2x-3x annual commission versus 1.5x-2x for personal lines.

Q: What's a niche commercial book worth?

A: Specialty books (contractors, transportation, hospitality, professional liability) can command premium multiples above the standard commercial range. The expertise creates a barrier to entry that protects retention and supports higher valuations from PE and strategic acquirers.

Q: Can I buy a mixed book instead of choosing?

A: Mixed books fall between the two ranges, with the commercial percentage pushing the multiple up. A 50/50 book might price at 1.8x-2.4x. This is often the smartest play for buyers who want commercial exposure without the full complexity of a pure commercial acquisition.

Sources & References

- Peak Business Valuation, Valuation Multiples for an Insurance Brokerage

- Sica Fletcher, Insurance Agency Valuation Rule of Thumb

- OPTIS Partners / Insurance Journal, P&C and Benefits Brokerage M&A: 750+ Deals in 2024

- MarshBerry, How to Think About Value

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.