What Pushes Insurance Agency Multiples Higher Than Average

What drives insurance agency multiples from 4x to 8x EBITDA: organic growth, retention above 90 percent, EBITDA margin, owner dependency, and commercial-lines mix.

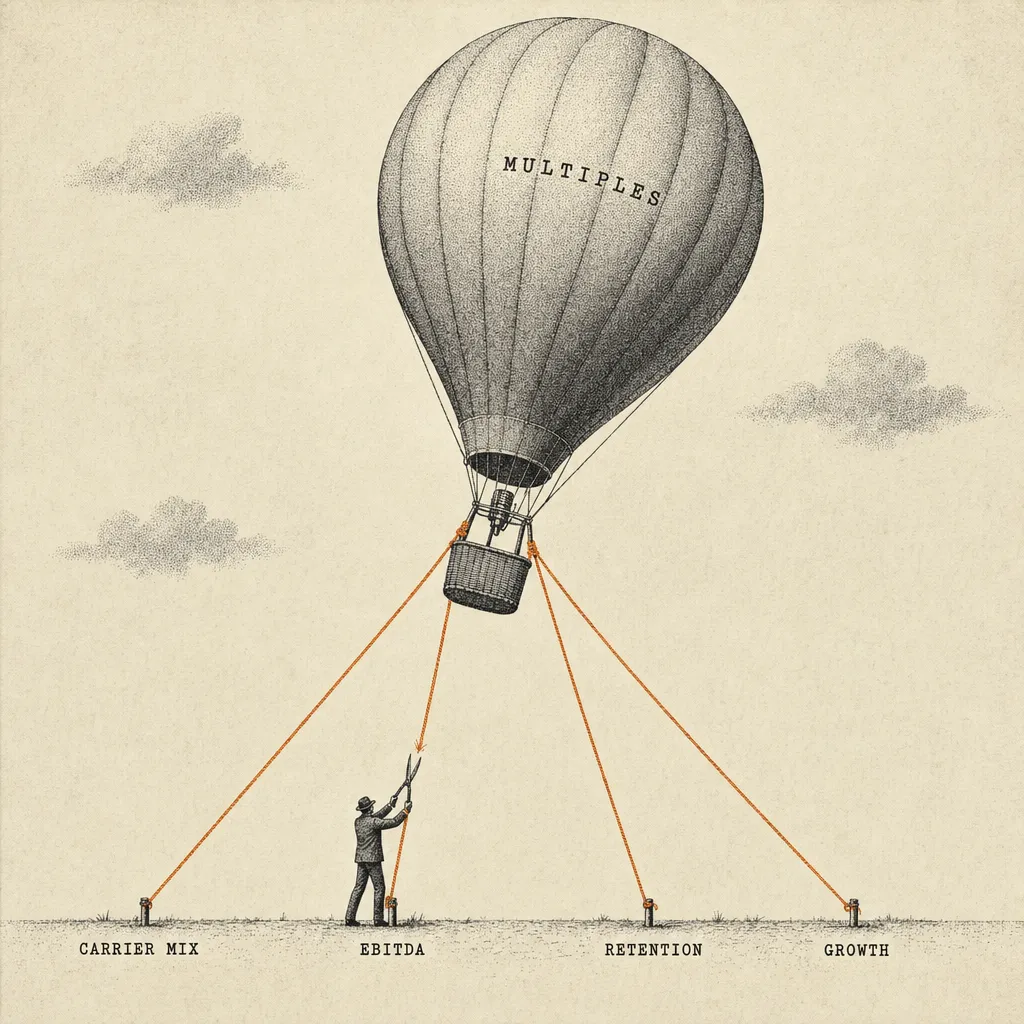

The factors that push agency multiples from 4x to 8x EBITDA: organic growth rate, retention above 90 percent, EBITDA margin above 25 percent, low owner dependency, documented systems, and commercial-lines mix. Two agencies at identical revenue can fetch double or half the multiple depending on these inputs.

Two agencies. Both doing $1 million in revenue. Both independent. Both profitable. One sells for $2 million. The other sells for $4.5 million. Same market, same year, same general type of business.

What happened?

Multiples happened. And the difference between a lower multiple and a premium one isn't luck or timing, it's a specific set of factors that acquirers evaluate, and that many agency owners don't focus on until they're close to exit.

How Does Organic Growth Rate Move the Agency Multiple?

Consistent organic growth is one of the strongest drivers of valuation multiples. An agency demonstrating strong double-digit organic growth is fundamentally more attractive to acquirers than one growing at low single digits, even if the slower agency has higher current revenue.

Growth signals market demand, effective operations, and a book that isn't just coasting on renewals. PE firms especially love growth because they're buying future cash flow, not just today's earnings. Strong organic growth can materially improve your multiple, it signals to acquirers that the agency has momentum and scalable operations.

The flip side: flat growth over several years typically signals to acquirers that the business has limited upside, which tends to compress multiples.

These ranges align with third-party data: Peak Business Valuation reports average revenue multiples of 1.82x-2.33x for insurance agencies, while ExitWise documents commission multipliers from 1.0x-3.5x depending on agency quality and size. For the underlying methodology (revenue vs EBITDA vs SDE) see our insurance agency valuation guide.

How Much Does Retention Rate Move the Agency Multiple?

Retention is the silent killer of agency valuations. The difference between 90 percent retention and 95 percent retention sounds like 5 percentage points. Over five years, it's the difference between keeping half your book and keeping three-quarters of it.

Sophisticated acquirers model retention forward. An agency with 95 percent retention has predictable, stable cash flow. An agency with 85 percent retention has a declining book that requires constant new business just to stay flat. One is a premium asset. The other is a treadmill.

How Does EBITDA Margin Move the Agency Multiple?

An agency doing $1 million in revenue at a 15 percent margin produces $150,000 in EBITDA. At a 7x multiple, it's worth just over $1 million. The same revenue at a 30 percent margin produces $300,000 in EBITDA. At 7x, that's $2.1 million. At 8x, which the higher-margin agency is more likely to command, it's $2.4 million.

Every point of margin is a multiplier on your exit price. The agencies hitting 25 to 30 percent margins aren't working twice as hard. They've built better systems, optimized their carrier mix, and invested in technology that reduces servicing costs. Our EBITDA margin benchmarks guide walks through where margin typically gets eaten and how to claw it back.

Why Does Owner Dependency Drag the Agency Multiple Down?

Here's a question acquirers consistently raise: what happens if the owner disappears for 90 days? If the answer is "the business continues normally," you've got a premium asset. If the answer is "it falls apart," you've got a job wearing a business costume.

Agencies that run without the owner, that have documented processes, trained staff, distributed client relationships, and a second-in-command who can actually command, sell at higher multiples, per MarshBerry, which identifies management depth as a key valuation driver. The agency is the asset, not the person.

How Do Technology and Systems Lift the Agency Multiple?

Modern tech stack signals operational maturity. An agency running on a current AMS with integrated comparative raters, automated renewals, and digital client servicing is worth more than one running on spreadsheets and Post-it notes.

Acquirers increasingly evaluate technology because it signals scalability. Can they bolt this agency onto their existing platform? Can they grow it without proportionally adding staff? Modern technology says yes. Legacy systems say "this is going to cost us."

What Is the Commercial-Lines Premium on Agency Multiples?

Personal lines agencies and commercial lines agencies serve different markets and command different multiples. Commercial books tend to have higher revenue per account, deeper relationships, and lower client turnover. Sica Fletcher and MarshBerry data confirm that commercial-weighted agencies command higher multiples.

In our marketplace experience, books with meaningful commercial components tend to command stronger multiples than purely personal lines agencies. Niche commercial specialties like contractors insurance, transportation, or professional liability can push multiples higher still.

MarshBerry's year-end data confirms this trend: private capital-backed buyers represented 73.5% of all brokerage transactions through November 2024, with aggregate deal values increasing 72% to $49.4 billion despite fewer total transactions, per Deloitte.

Risk & Insurance reports that the insurance brokerage sector maintained 476 deals in 2024, nearly matching 2023's 485, but the average deal value spiked 207% due to mega-transactions like the $7.6B Truist Insurance Holdings deal.

"Agencies usually sell between 8x-12x EBITDA, so conservatively multiplying by 7x-11x can give you a better idea of the high and low ends of your possible valuations." Sica Fletcher, #1 S&P-Ranked Insurance M&A Advisory Firm (Sica Fletcher)

How Do These Factors Compound to Push the Multiple Higher?

The agencies that sell at the high end of the EBITDA range, Sica Fletcher documents 8x-12x for strong performers, aren't doing one of these things well. They're doing all of them. Growing organically, retaining at 95 percent plus, running efficient operations, not depending on the owner, using modern technology, and building a diversified book with commercial depth.

These factors are largely within the owner's control and are driven by strategic decisions as much as effort, decisions that compound over time when made with the exit in mind. For the structured execution plan, see our 3-year playbook for preparing your agency for sale.

Frequently Asked Questions

Q: How does retention affect my multiple?

A: Retention is the single biggest lever. The gap between 90% and 95% retention compounds over a buyer's hold period into keeping most of the book versus half of it. Sub-90% retention forfeits any shot at premium multiples.

Q: Should I pay myself less to increase EBITDA before selling?

A: Only if you're overpaying relative to market. Buyers will normalize owner comp either way, the clean win is pulling personal expenses off the P&L, which directly raises EBITDA and multiplies 6-10x at exit.

Q: Why did my agency come in lower than I expected?

A: Usually owner dependency, undocumented systems, or a personal-lines-heavy book. Commercial books typically command 20-40% higher multiples than personal lines, and agencies that can run 90 days without the owner get the premium tier.

Q: Do agencies really sell for 8-12x EBITDA?

A: Only platform-quality ones. Agencies hitting 8-12x typically combine 25%+ EBITDA margins, 93%+ retention, organic growth, documented systems, modern technology, and producer-driven (not owner-driven) revenue.

Q: Is 2x revenue a fair price for my book?

A: 2x is near the top of the revenue-multiple range. Earning it requires 90%+ retention, a commercial-heavy or niche book, transferable carrier appointments, and clean financials. See how to value a P&C insurance agency for the full framework.

Sources & References

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.