Insurance Agency EBITDA Margins: Where Do You Rank?

Insurance agency EBITDA margin benchmarks: top quartile hits 25 to 30 percent, average sits 15 to 20 percent. Where margin gets eaten and how to close the gap.

Top agencies hit 25 to 30 percent EBITDA margins; the average sits at 15 to 20 percent. Margin loss usually comes from producer comp drift, owner overhead bundled into the P&L, and tech subscription sprawl. Each margin point lifts the enterprise multiple by a roughly proportional amount.

There's a number that separates lifestyle agencies from enterprise-value agencies, and many owners don't track where they fall on the spectrum.

EBITDA margin, what your agency actually earns as a percentage of revenue after operating expenses, is one of the most important metrics for determining your agency's value. MarshBerry identifies profitability as a primary driver of valuation multiples, alongside growth and management depth.

What Are the EBITDA Margin Benchmarks Across P&C Agencies?

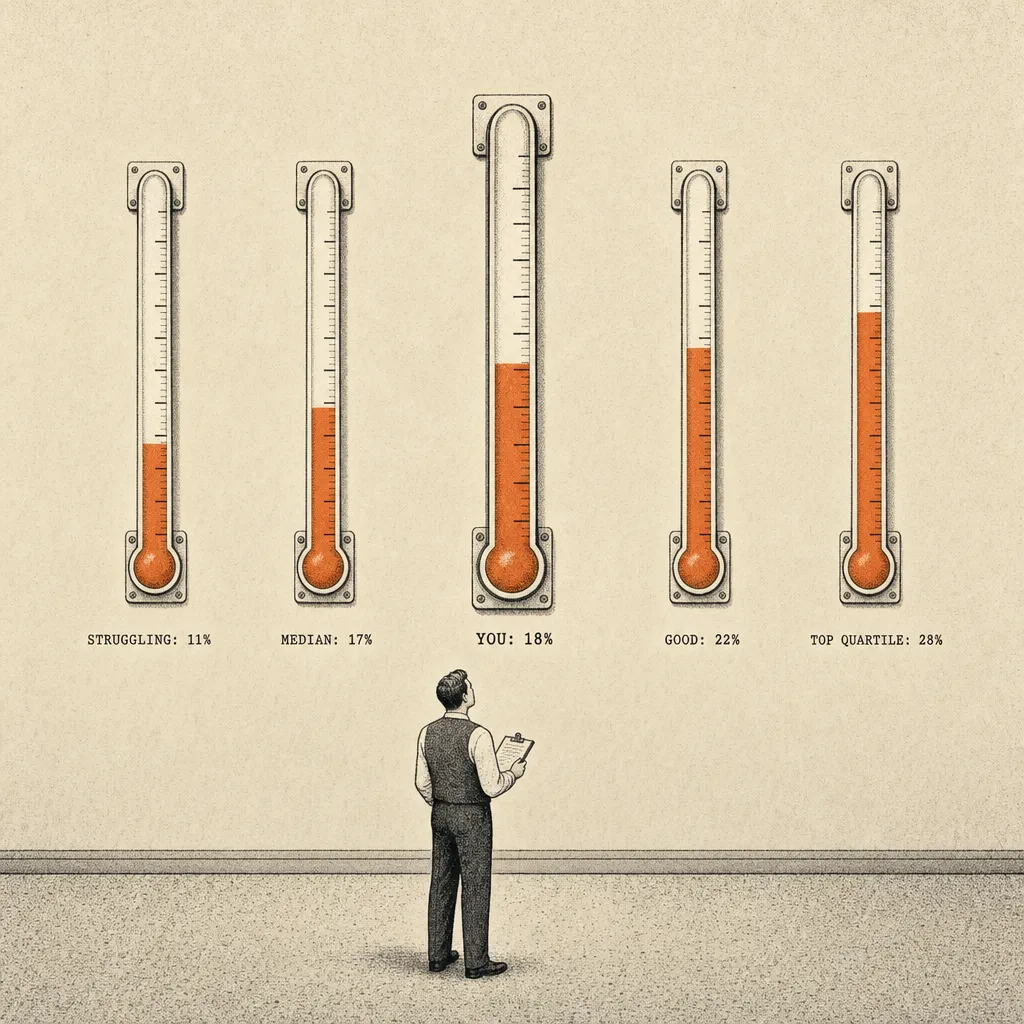

The insurance agency industry average EBITDA margin sits at 15 to 20 percent. If you're in that range, you're at the industry average, but there may be significant room to increase enterprise value.

Top-performing independent agencies, the ones PE firms fight over, run at 25 to 30 percent margins or higher. MarshBerry confirms these benchmarks: top independent firms achieve EBITDA margins of 25-30%+, while the industry average sits at 15-20%. That gap between 18 percent and 28 percent might not sound like much, but run the math on what it means for your exit.

An agency doing $800,000 in revenue at an 18 percent margin produces $144,000 in EBITDA. At a 7x multiple, the agency is worth roughly $1 million. (Insurance Journal) The same agency at a 28 percent margin produces $224,000 in EBITDA. At 8x, MarshBerry confirms that stronger profitability commands higher multiples, that's $1.79 million.

Same revenue. Same market. Same clients. An $800,000 difference in enterprise value driven entirely by operational efficiency. For the other factors that compound with margin to push multiples higher, see what drives insurance agency multiples higher.

Where Does Agency EBITDA Margin Actually Get Eaten?

Most agency owners know they should be more profitable. Fewer understand where the margin actually disappears.

Staffing is the biggest line item. Per Agency Brokerage and Tony Caldwell's agency benchmarking, staffing efficiency is the largest controllable driver of agency margins, overstaffing and inflated operating expenses directly reduce EBITDA. This doesn't mean cutting people, it means making sure every role produces enough value to justify its cost, and using technology to handle tasks that don't require a human.

Carrier mix matters more than most agents realize. Some carriers pay better commissions for the same products. Some have bonus structures that kick in at premium thresholds you're close to hitting. Optimizing your carrier appointments, and strategically placing business where it rewards you best, can add meaningful margin without writing a single new policy. Agency Focus identifies carrier mix optimization as a key operational lever for independent agencies.

Technology costs money upfront but saves it over time. Modern systems reduce per-policy servicing costs, Agency Brokerage notes that technology utilization is a primary factor in agency profit margin variation. Automated renewals, digital client portals, and integrated rating engines reduce the human hours per policy, which directly improves margin.

How Does EBITDA Margin Multiply Enterprise Value at Exit?

Here's what makes margin obsession worthwhile: every dollar of additional EBITDA doesn't just add a dollar of value. It adds six to ten dollars, depending on your multiple. (Sica Fletcher documents EBITDA multiples ranging from 8 to 12x for well-performing independent agencies.)

If you can increase your EBITDA margin from 18 percent to 25 percent on $800,000 in revenue, you're adding $56,000 in annual earnings. At a 7x multiple, that $56,000 becomes $392,000 in additional enterprise value. You didn't write a single new policy. You didn't spend more on marketing. You ran the same business more efficiently, and your exit price went up by nearly $400,000.

This is the core of the PE acquisition playbook, MarshBerry documents how operational improvement drives valuations. Every point of margin added before exit gets multiplied by the EBITDA multiple. Agency owners can apply the same logic to their own operations.

What Separates a Lifestyle Agency From an Enterprise Agency on Margin?

There's nothing wrong with running a lifestyle agency. Taking home a good income, working reasonable hours, serving your community. That's a perfectly valid choice.

But understand that a lifestyle agency and an enterprise-value agency are different things, and they're valued differently. The lifestyle agency optimizes for owner income today. The enterprise agency optimizes for business value at exit. The difference in approach, in how you staff, invest in technology, manage expenses, and think about growth, can be substantial, as illustrated by the margin math above.

Most agents never make a conscious choice between these two paths. They default into one or the other based on habits and inertia. The ones who choose deliberately, who decide what they're building and why, end up in a fundamentally stronger position regardless of which path they pick.

Know your margin. Know where you stand. Then decide if that's where you want to be. If you're planning an exit, our 3-year playbook for preparing your agency for sale walks through the margin improvements that move the needle most.

"Failing to drive operational improvement within your firm can cause you to leave a lot of money on the table." Phil Trem, President of Financial Advisory at MarshBerry (MarshBerry)

Frequently Asked Questions

Q: Should I pay myself less to increase EBITDA before selling?

A: Only if you're overpaying relative to market. Buyers normalize owner compensation anyway, underpaying yourself just means they add the cost back. The real move is pulling personal expenses off the books at least 3 years before sale.

Q: What multiple should I use, revenue or EBITDA?

A: If your EBITDA margin is 25%+, push for an EBITDA multiple because it rewards profitability. If your margin is sub-20% or your financials are noisy, a revenue multiple is often more favorable. See revenue multiple vs EBITDA multiple.

Q: Do agencies really sell for 8-12x EBITDA?

A: Only platform-quality agencies with $2M+ EBITDA, strong margins, and growth hit that range. 12.5x-14.5x is reserved for $5M+ EBITDA platforms. Sub-$2M EBITDA agencies typically transact at 6x-10x or on revenue multiples.

Q: How does retention affect my multiple?

A: Retention and EBITDA margin travel together. A book with 95% retention and 25%+ margin can defend top-of-range multiples; the same EBITDA with 80% retention gets discounted because the cash flow stream is riskier. See what drives insurance agency multiples higher.

Q: Why did my agency come in lower than I expected?

A: Most often it's EBITDA margin dragging down the headline. Raising margin from 18% to 25% on an $800K revenue agency can add roughly $400K to enterprise value without writing a single new policy. See agency valuation mistakes.

Sources & References

- MarshBerry: How to Think About Value

- Insurance Journal: EBITDA Multiples in Agency M&A

- Sica Fletcher: Insurance Agency Valuation Rule of Thumb

- Peak Business Valuation: Valuation Multiples for an Insurance Agency

- Deloitte: Insurance M&A Outlook

Related reading: agency marketing budget benchmarks.

How Do You Run Margin Math When Owner Comp Is Mixed With Operations?

Strip owner compensation back to a fair market replacement salary before computing EBITDA. Buyers do this in their first model anyway, and the gap between your reported margin and the buyer-normalized margin is where 80 percent of valuation disputes start.

Written by licensed property and casualty agency operators on the Insurance Dudes M&A Desk. Insurance Agency Trader is US-based, serving independent and captive agency owners across the United States.

Editorial process: every post is reviewed against our published valuation math and current market data before it ships, and updated when the numbers move. Corrections: email craig@insuranceagencytrader.com and we will fix errors promptly.